March 30, 2020

Over the last few weeks, the DJIA declined significantly. The DJIA price level declined 37% from its peak on February 12, 2020 to the most recent low on March 23, 2020. Valuation measures can give us an idea of how far prices might fall near term by looking at changes in valuation levels in past declines. My original note about valuation is in: https://marketresilience.blogspot.com/2020/03/update-march-22-2020.html, in the section titled: "The DJIA May Be in the Bargain Basement."

This note provides additional data.

Price-to-Book Ratio Changes in the Great Depression

The Price-to-Book ratio for major market sectors in during the 1930s declined from their highs in 1929 to about 50% of the prior high values by 1930. This information comes from "The Crash and Its Aftermath: A History of Securities Markets in the United States, 1929-1933," by Barry Wigmore (1985). The decline took place over a longer time than the recent Corona decline, and there may have been write-downs in book value during that longer period that make this comparison less meaningful.

As comparison, the Price-to-Book ratio of the DJIA declined to 2.9 as of March 22, 2020 from a high of 4.4 just a month earlier. This represents a drop to 66% of its prior high value.

Price-to-Earnings Ratio Changes in 1987

During the 1987 Crash the DJIA price level declined about 30% from August 25 to October 19. I can locate only Price-to-Earnings ratio information for this decline. Over the same time period, the DJIA's Price-to-Earnings ratio had declined to 67% of its prior high value.

This information is from the New York Times. https://www.nytimes.com/1987/11/27/business/economic-scene-taking-a-look-at-p-e-ratios.html

As a comparison, the DJIA Price-to-Earnings ratio declined to 65% of its prior high level from February 12, 2020 to March 23, 2020.

Summary

This information suggests that the recent decline has already produced low valuations, low enough by historical standards to attract bargain-hunting investors. I believe the information in the original note linked above and this additional note is relevant for the immediate time period. Please note that earnings and book values will certainly change (decline) as a result of the pandemic and economic decline. As we start seeing additional deterioration in the real economy, other valuation assessments might be needed to give perspective.

As you know, the MRI-based process does not include valuation information because it is difficult to obtain accurate historical information. But I do refer to it on a regular basis for market context, especially during times of market stress.

Focused 15 Investing

3/27/2020

Research Note: Three Market Scenarios and Possible Responses

As you may know, my views on forward looking scenarios do not have an impact on the target weights, but they do influence my review of portfolio designs as I evaluate whether there is a change in the economy or markets that requires a shift in their designs. As an example, the recent price decline was a shock to many investors and affected their short-term risk tolerances. I adjusted the model portfolio lineup and my communication to make it easier to adjust the aggressiveness of one's account.

The model portfolios currently hold US 10y Treasury bonds also because of their quality and liquidity. In times of crisis, quality and liquidity make it easy to adjust our asset allocations and to remove money from the market. We do not hold corporate bonds because they may be difficult to trade in times of stress.

I am currently evaluating three different scenarios for the path ahead to determine what, if any, changes might be made to model portfolio design to accommodate scenarios more extreme than the one I consider most likely.

The Likely Scenario - Economic Activity Constrained to "Virus Time"

Current expectations:

The fact that we just recently had a major financial crisis (2007-9) with bailouts and stimulus packages is important to the current situation. The Global Financial Crisis was just over ten years ago as opposed to something we could only read about in history books. Many of the same people and institutions have been involved in both crises and I believe there is general dissatisfaction with how the past rescues of big corporations and financial institutions failed to benefit the consumer as much as needed. In the subsequent years, interest rates have been pushed lower and lower to encourage growth.

But the debt load carried by the economy has expanded (because of low rates) to the point where any increase in interest rates has a devastating effect on both corporations and consumers. We seem to have come to the end of the long trend toward lower interest rates that started in the 1980s when short term rate (2-year treasuries) was 16.7% in September of 1981 to the current rate of 0.23% (March 2020). While Japan has had negative interest rates for a few years, low rates distort corporate and individual investment and borrowing decisions.

This current crisis may be a way of clearing out the debt load and resetting debt loads and interest rates to a more healthy and sustainable relationship. Thus, the pandemic can be thought of as precipitating important changes that would have come about without the virus but in a perhaps slower and probably less comprehensive manner.

If this scenario is valid, our current lineup of model portfolios is likely to navigate the 2020 recovery reasonably well. The design of the current model portfolios is based on analyses of prior recessions and market crashes and their recoveries. Our portfolios emphasize the DJIA because of the quality and liquidity of the companies it contains. Should there be widespread bankruptcies in the broader market, the DJIA companies generally considered strong and some of the DJIA companies may actually grow stronger as they absorb customers from the competition. For reference, the top 10 holdings of the DJIA are:

The Likely Scenario - Economic Activity Constrained to "Virus Time"

Current expectations:

- Unemployment will spike dramatically over the near term and stay high for many months.

- Bankruptcies will spike as well.

- The Federal Reserve and its counterparts around the world have already stated emphatically that they will do “whatever it takes” to limit the damage of this crisis. Their actions have been consistent with their statements. Additional actions are expected.

- Congress and the President have enacted stimulus packages and have promised more

- Social distancing will continue in some form until a vaccine is developed in 12+ months. Until that time, travel and entertainment, dining out, and shopping for non-essentials will be severely limited.

- Economic activity will begin to resume when there is an effective and scalable way to test for antibodies, which can identify people immune to Covid-19 who can safely return to work. The antibody test is some months away.

- More people are working effectively at home than would have been possible a few decades ago or certainly during the Spanish Flu in 1918-9. Economic activity is continuing during lockdown, which may be the source of some positive surprises.

- The level of bad news in the market will likely be higher in the US when death rates spike over the next several weeks, employment reports come out, and the scale of the immediate economic damage becomes more apparent.

- Investors will see some light at the end of the tunnel as Europe moves through its curve of infection, mortalities decrease, and people return to work. Asia is more advanced in that sequence. India and South America may be behind the US.

The fact that we just recently had a major financial crisis (2007-9) with bailouts and stimulus packages is important to the current situation. The Global Financial Crisis was just over ten years ago as opposed to something we could only read about in history books. Many of the same people and institutions have been involved in both crises and I believe there is general dissatisfaction with how the past rescues of big corporations and financial institutions failed to benefit the consumer as much as needed. In the subsequent years, interest rates have been pushed lower and lower to encourage growth.

But the debt load carried by the economy has expanded (because of low rates) to the point where any increase in interest rates has a devastating effect on both corporations and consumers. We seem to have come to the end of the long trend toward lower interest rates that started in the 1980s when short term rate (2-year treasuries) was 16.7% in September of 1981 to the current rate of 0.23% (March 2020). While Japan has had negative interest rates for a few years, low rates distort corporate and individual investment and borrowing decisions.

This current crisis may be a way of clearing out the debt load and resetting debt loads and interest rates to a more healthy and sustainable relationship. Thus, the pandemic can be thought of as precipitating important changes that would have come about without the virus but in a perhaps slower and probably less comprehensive manner.

If this scenario is valid, our current lineup of model portfolios is likely to navigate the 2020 recovery reasonably well. The design of the current model portfolios is based on analyses of prior recessions and market crashes and their recoveries. Our portfolios emphasize the DJIA because of the quality and liquidity of the companies it contains. Should there be widespread bankruptcies in the broader market, the DJIA companies generally considered strong and some of the DJIA companies may actually grow stronger as they absorb customers from the competition. For reference, the top 10 holdings of the DJIA are:

- Apple Inc

- UnitedHealth Group Inc

- Home Depot Inc/The

- Goldman Sachs Group Inc/The

- Visa Inc

- McDonald's Corp

- Microsoft Corp

- Johnson & Johnson

- 3M Co

- Boeing Co/The

The model portfolios currently hold US 10y Treasury bonds also because of their quality and liquidity. In times of crisis, quality and liquidity make it easy to adjust our asset allocations and to remove money from the market. We do not hold corporate bonds because they may be difficult to trade in times of stress.

A More Positive Scenario

I can imagine a more positive outcome for the global economy from the current events. Many individuals and businesses will suffer and be forced into bankruptcy. In this scenario, the changes happen quickly. There will be some form of debt forgiveness, perhaps in the form of student loan forgiveness or mortgage relief. Reduced debt load among consumers and businesses and the global economic stimulus will encourage rapid economic growth. Fiscal stimulus will help rebuild infrastructure faster than would have otherwise occurred and provide future efficiencies. Surviving business will grow quickly with a lower debt load. In the next couple of years, we may begin to see hints of inflation.

If this scenario becomes more likely, it may be helpful to incorporate inflation-linked bonds as a component. I have been running inflation signals sets since 2007 and can incorporate them if needed.

A More Negative Scenario

Even though we are seeing an extremely fast response from governments around the world, the inevitable economic contraction may be extremely difficult for many businesses and sectors of the economy. They will not muddle through easily. Individuals and business bankruptcies will grow more than expected right along with unemployment rate. Financial stress and dislocation will reverberate through the global economy for many quarters despite the speed and magnitude of the government response. Economic growth will not rebound evenly throughout the US or global economies.

I am evaluating variations of the current model portfolios that seeks to have more exposure to the parts of the economy that may benefit during the more negative scenario. I tentatively call it the 2020 Recovery model portfolio and its structure is based on the Diamond-Onyx Mixes. It uses existing signal sets (developed over 7 years ago), which makes the historical simulations far less vulnerable to back-fitting the solution to the time period just experienced.

The thrust of the modification is to have greater exposure to consumer staples companies, technology companies, and health care companies. These sectors may experience better growth than other areas of the market.

Consumer Staples companies tend to have steady business in difficult economic times. They may get a boost as more people eat at home and seek to make life at home comfortable and pleasant. We currently use the ETF XLP for Consumer Staples companies in the Onyx mixes. The modification would increase the allocation to this ETF. The top 10 holdings of this ETF are:

If this scenario becomes more likely, it may be helpful to incorporate inflation-linked bonds as a component. I have been running inflation signals sets since 2007 and can incorporate them if needed.

A More Negative Scenario

Even though we are seeing an extremely fast response from governments around the world, the inevitable economic contraction may be extremely difficult for many businesses and sectors of the economy. They will not muddle through easily. Individuals and business bankruptcies will grow more than expected right along with unemployment rate. Financial stress and dislocation will reverberate through the global economy for many quarters despite the speed and magnitude of the government response. Economic growth will not rebound evenly throughout the US or global economies.

I am evaluating variations of the current model portfolios that seeks to have more exposure to the parts of the economy that may benefit during the more negative scenario. I tentatively call it the 2020 Recovery model portfolio and its structure is based on the Diamond-Onyx Mixes. It uses existing signal sets (developed over 7 years ago), which makes the historical simulations far less vulnerable to back-fitting the solution to the time period just experienced.

The thrust of the modification is to have greater exposure to consumer staples companies, technology companies, and health care companies. These sectors may experience better growth than other areas of the market.

Consumer Staples companies tend to have steady business in difficult economic times. They may get a boost as more people eat at home and seek to make life at home comfortable and pleasant. We currently use the ETF XLP for Consumer Staples companies in the Onyx mixes. The modification would increase the allocation to this ETF. The top 10 holdings of this ETF are:

- Estee Lauder Cos Inc/The

- Mondelez International Inc

- Coca-Cola Co/The

- Procter & Gamble Co/The

- Walmart Inc

- JM Smucker Co/The

- Altria Group Inc

- Sysco Corp

- Kraft Heinz Co/The

- Archer-Daniels-Midland Co

The 2020 Recovery would obtain greater technology exposure by having an allocation to the ETF QQQ, which tracks the NASDAQ 100 index. The Nasdaq 100 Index is composed of 100 of the largest international and domestic companies, excluding financial companies, that are listed on the Nasdaq stock exchange, based on market capitalization. Therefore, QQQ is heavily weighted toward large-cap technology companies and is often viewed as a snapshot of how the technology sector is trading. The growth of online commerce, new technological solutions to address workplace challenges (e.g. remote working and online meetings and classes), the growing need to provide social connections in in a socially distanced world, and investment in new technologies to solve emerging problems will likely boost the NASDAQ. The top 10 holdings of QQQ are:

Health Care companies would be included in the Covid 2020 Recovery model portfolio. They are likely to get a direct boost from consumer and government spending because of the pandemic. These companies might also be affected by changes in the healthcare system as we move through the recovery. Should this sector deteriorate as an investment, it may be removed from the model portfolio. We would have an allocation to the ETF XLV. Its top 10 holdings are:

The resulting model portfolio has similar characteristics of the Onyx mixes currently offered, although it holds more ETFs. While the design of the existing model portfolios considers a very long frame based on historical experiences, the Covid 2020 Recovery portfolio is more thematic and is more likely to be modified over time.

After additional testing, I will report my findings on this evaluation.

- MICROSOFT CORP

- APPLE INC

- AMAZON.COM INC

- ALPHABET INC-CL A & C

- FACEBOOK INC-CLASS A

- INTEL CORP

- PEPSICO INC

- CISCO SYSTEMS INC

- COMCAST CORP-CLASS A

- NETFLIX INC

Health Care companies would be included in the Covid 2020 Recovery model portfolio. They are likely to get a direct boost from consumer and government spending because of the pandemic. These companies might also be affected by changes in the healthcare system as we move through the recovery. Should this sector deteriorate as an investment, it may be removed from the model portfolio. We would have an allocation to the ETF XLV. Its top 10 holdings are:

- Johnson & Johnson

- UnitedHealth Group Incorporated

- Merck & Co., Inc.

- Pfizer Inc.

- Abbott Laboratories

- Bristol-Myers Squibb Company

- Amgen Inc.

- Medtronic Plc

- Eli Lilly and Company

- Thermo Fisher Scientific Inc.

The resulting model portfolio has similar characteristics of the Onyx mixes currently offered, although it holds more ETFs. While the design of the existing model portfolios considers a very long frame based on historical experiences, the Covid 2020 Recovery portfolio is more thematic and is more likely to be modified over time.

After additional testing, I will report my findings on this evaluation.

3/26/2020

Research Note: Model Portfolio Returns During Covid Crash 1/1/2020 thru 3/20/2020

The recent market decline has been dramatic. The last month has been a real-time stress test of the design of the Focused 15 Investing model portfolios.

I'd like to review how the popular model portfolios held up during this period. The graphic quality of the tables below is not good so I will discuss the columns of the table in detail for the DJIA. A large version of the table appears toward the end of this note.

Column A shows the annualized rate of return for the DJIA for the 5-plus years from 7/18/2014 (the first week of the Focused 15 Investing publications) through 3/20/2020 (last Friday). The DJIA returned 4.7% per year, on average, over that period. A higher percentage is better.

Column B shows the variability of those DJIA returns, 16.4%. Here, a lower value is better.

Column C shows the ratio of those two numbers. A higher ratio is better. The Return-to-Variability ratio for the DJIA over this 5+-year time period has been 0.3.

Column D shows the year-to-date (YTD) return for the DJIA. The return has been -33%.

Column E shows how much of the DJIA history of returns has been wiped out by the recent decline. Last Friday's price was the same level that the DJIA last had on 4/21/2017, 152 weeks ago.

Finally, column F shows the longer-term performance of the DJIA, beginning 1/7/2000. Its annualized return for the last 20 years has been 5.1%.

As you know, the DJIA is very important to the model portfolios and is a useful reference for comparison.

The chart below adds the Diamond (sg131) model portfolio to the information above.

Column A, row 2 shows Diamond (sg131)’s annualized return of 9.3%. This compares favorably to the 4.7% annualized return for the DJIA.

Column B shows the Variability. Diamond has Variability of 16.5%, which is very close to the variability of the DJIA.

The Return-to-Variability ratio is 0.6, which compares favorably to the DJIA's ratio of 0.3. Our goal is to get higher return for the same variability and this statistic reinforces that we are moving toward that goal, even in a down market.

Regarding the YTD loss (Column D), the Diamond model portfolio returned -32%, similar to the loss for the DJIA. The Diamond model portfolio has given up 131 weeks of returns (Column E). The level as of last Friday is where Diamond was on 9/15/2017.

Column F shows that Diamond model portfolio returned 18.7% annualized over the past 20 years - even after the recent decline. Of course, much of this history represents a historical simulation and it is best to consider this number a general guide of the return potential of the model portfolio - it is quite a bit higher than the return of the DJIA.

The table below adds some of the reference portfolios in the weekly publications.

As of last Friday, the Vanguard fund VASGX (row 10) returned 2.7%, annualized, over the 5+ years since 7/18/2014. VASGX holds 80% stocks and 20% bonds. Its year-to-date return is -22%. This is a smaller loss than the DJIA or Diamond (sg131). VASGX's level last Friday is where it was 4/28/2017, 151 weeks ago. This is about the same as what the DJIA has done and more than Diamond (sg131)'s 131 weeks. VASGX's annualized return since 2000 is 4.0%.

I included the Russell LifePoints Fund (RALAX). I worked at Russell for several years and their investment strategy (multi-manager, multi-style diversification) is used by many investment firms around the world. RALAX had a return for this year of -29%, which is not far from the loss of the DJIA and the Diamond model portfolio. Yet its annualized return since 7/18/2014 is -1.4%. It gave up all the returns it has earned for 213 weeks (since 2/17/2016). Its long-term returns (since Jan 2000) have been 4.1%. The returns for funds listed under "Funds for Performance Comparison" reflect fund fees, which vary from fund to fund.

The table below adds other popular Focused 15 Investing model portfolios.

A few points are worth noting.

I'd like to review how the popular model portfolios held up during this period. The graphic quality of the tables below is not good so I will discuss the columns of the table in detail for the DJIA. A large version of the table appears toward the end of this note.

Column A shows the annualized rate of return for the DJIA for the 5-plus years from 7/18/2014 (the first week of the Focused 15 Investing publications) through 3/20/2020 (last Friday). The DJIA returned 4.7% per year, on average, over that period. A higher percentage is better.

Column B shows the variability of those DJIA returns, 16.4%. Here, a lower value is better.

Column C shows the ratio of those two numbers. A higher ratio is better. The Return-to-Variability ratio for the DJIA over this 5+-year time period has been 0.3.

Column D shows the year-to-date (YTD) return for the DJIA. The return has been -33%.

Column E shows how much of the DJIA history of returns has been wiped out by the recent decline. Last Friday's price was the same level that the DJIA last had on 4/21/2017, 152 weeks ago.

Finally, column F shows the longer-term performance of the DJIA, beginning 1/7/2000. Its annualized return for the last 20 years has been 5.1%.

The chart below adds the Diamond (sg131) model portfolio to the information above.

Column A, row 2 shows Diamond (sg131)’s annualized return of 9.3%. This compares favorably to the 4.7% annualized return for the DJIA.

Column B shows the Variability. Diamond has Variability of 16.5%, which is very close to the variability of the DJIA.

The Return-to-Variability ratio is 0.6, which compares favorably to the DJIA's ratio of 0.3. Our goal is to get higher return for the same variability and this statistic reinforces that we are moving toward that goal, even in a down market.

Regarding the YTD loss (Column D), the Diamond model portfolio returned -32%, similar to the loss for the DJIA. The Diamond model portfolio has given up 131 weeks of returns (Column E). The level as of last Friday is where Diamond was on 9/15/2017.

Column F shows that Diamond model portfolio returned 18.7% annualized over the past 20 years - even after the recent decline. Of course, much of this history represents a historical simulation and it is best to consider this number a general guide of the return potential of the model portfolio - it is quite a bit higher than the return of the DJIA.

The table below adds some of the reference portfolios in the weekly publications.

I included the Russell LifePoints Fund (RALAX). I worked at Russell for several years and their investment strategy (multi-manager, multi-style diversification) is used by many investment firms around the world. RALAX had a return for this year of -29%, which is not far from the loss of the DJIA and the Diamond model portfolio. Yet its annualized return since 7/18/2014 is -1.4%. It gave up all the returns it has earned for 213 weeks (since 2/17/2016). Its long-term returns (since Jan 2000) have been 4.1%. The returns for funds listed under "Funds for Performance Comparison" reflect fund fees, which vary from fund to fund.

The table below adds other popular Focused 15 Investing model portfolios.

- The Onyx mixes displayed good performance characteristics in the decline.

- The Diamond-Onyx Mix (sg218) shown on row 3 had a loss of 19% this year and has returned 9.7% annualized from 7/18/2014 through last Friday. It has given up only 60 weeks of its returns during the decline. As of last Friday, it was at the same level as on 1/25/2019, 60 weeks ago. The long-term simulated return (since Jan 2000) has been 16.4%.

- The Onyx sleeve is shown for reference, but it is not a separate model portfolio. It works best in partnership with the D5 signal set sleeve.

- The Onyx mixes shown in rows 5 and 6 use the DJIA-linked ETF "UDOW," which gives three times the return of the DJIA each day. The users of these model portfolios have multi-decade investment horizons. UDOW is aggressive and has achieved much higher return over the last 5+ years, yet these model portfolios experienced losses that are similar to those of the other model portfolios, suggesting that their structures held up during the recent decline.

- The model portfolio in row 6, Sapphire-Onyx Mix (sg299) had a loss of 36.9% this year, which is only four percentage points worse than the DJIA but has had an annualized return of 14.6% since 7/18/2014, compared to the DJIA's 4.7%. The model portfolio in row 6 is a green version of it.

3/24/2020

Weekly Note - March 24, 2020

ALERT: This is a good time to return to the target weights of the model portfolio you have selected. Attached is the weekly publication.

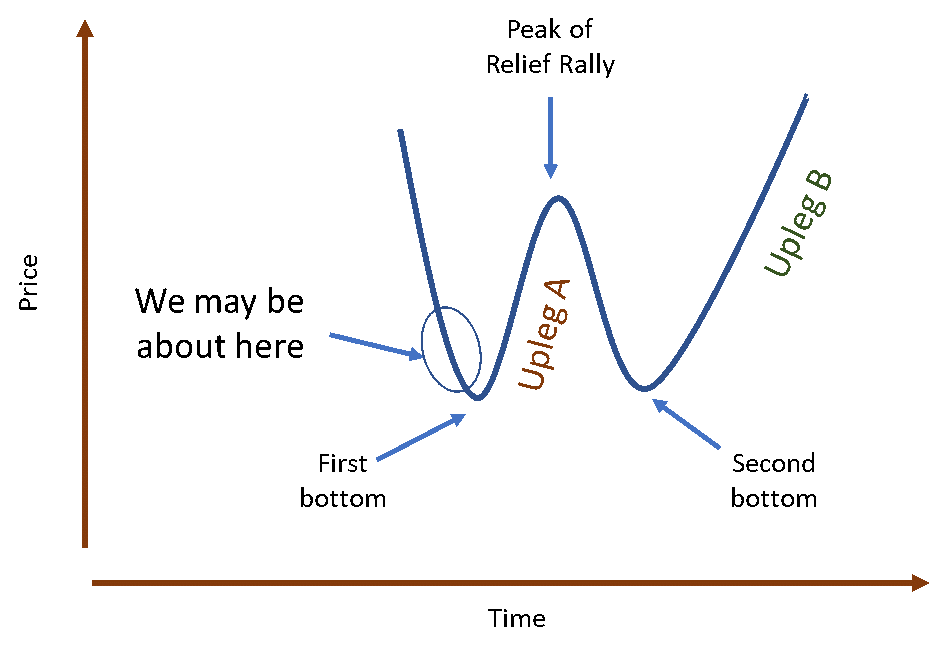

A Likely Beginning of a Relief Rally

I am sending the note out early this week because we may be beginning the relief rally I mentioned in my recent note.

Also, the target weights for the DJIA-linked ETFs (DIA, DDM, and UDOW), call for taking some money out of the stock market at the end of this week. When you move to the target weights this week (even before Friday if you choose), use the target weights on the attached weekly publication.

The DJIA’s move higher today is, I believe, a function of these factors in addition to the Micro MRI being at an extremely low level:

While there is much uncertainty in the real world, this may be the beginning of the Upleg A in the relief rally I mentioned in last blog post.

Now is a good time to move to the target weights of the model portfolio you used during the recent decline. When the relief rally moves up quickly, the fear of missing out on that price appreciation will be high. Be ready for that emotion, which I believe it is one of the strongest emotions that investors feel.

But I believe this is not the time to be more aggressive than model portfolio you used during the decline. There will be a better time in several weeks or maybe months for being more aggressive than you were during the decline. Of course, you are fee to use any model portfolio on the publication.

Recent blog post for more information on these topics.

Reduced Allocations to DJIA-linked ETFs

You may notice that the algorithms for the D5 signal set caused the allocation to the DJIA-linked ETFs (DIA, DDM, UDOW) to decrease this week. The reason driving this shift is that the market has not been responding as the algorithms expected, and the algorithms pull some money out. Basically, they are saying something is going wrong in the markets – take some money out and come back later. We may ultimately conclude that such reduced allocations were not useful in our current situation. But this signal has added value over the last 100 years, and we should follow it.

Following the Disciplines

As you know, I frequently advocate staying with the disciplines. I have seen many professional and non-professional investors lose money and their ability to focus by deviating from their established processes. I was evaluating professional investment managers for pension funds in the 1980s. The 1987 crash was interesting in that many of the investment indicators that investment professionals look at all day about the health of the markets went haywire. The indicators were erratic and in many cases contradictory. When the crash was over, we evaluated what happened and how managers navigated through the conflicting signals.

We found that those who followed their established processes did better. Those who saw the chaos and tried to reconcile all the conflicting indicators did not do as well. They responded to one indicator at one time and another indicator later, and they ended up trading aggressively to conform to what they saw most recently – believing recent information to be most reliable. I say this to disclose my bias in these situations. I feel like we are flying blind in many ways right now. But if we avoid being distracted by trying to reconcile all the conflicting information, I believe that we will navigate this more effectively.

A Likely Beginning of a Relief Rally

I am sending the note out early this week because we may be beginning the relief rally I mentioned in my recent note.

Also, the target weights for the DJIA-linked ETFs (DIA, DDM, and UDOW), call for taking some money out of the stock market at the end of this week. When you move to the target weights this week (even before Friday if you choose), use the target weights on the attached weekly publication.

The DJIA’s move higher today is, I believe, a function of these factors in addition to the Micro MRI being at an extremely low level:

- The likely passage of the stimulus bill

- Short-term investors unwinding their short positions (bets that the market will go down from here).

- Bargain hunters being attracted the valuations for the DJIA

- Possibly, the President moving to get everyone back to work

While there is much uncertainty in the real world, this may be the beginning of the Upleg A in the relief rally I mentioned in last blog post.

Now is a good time to move to the target weights of the model portfolio you used during the recent decline. When the relief rally moves up quickly, the fear of missing out on that price appreciation will be high. Be ready for that emotion, which I believe it is one of the strongest emotions that investors feel.

But I believe this is not the time to be more aggressive than model portfolio you used during the decline. There will be a better time in several weeks or maybe months for being more aggressive than you were during the decline. Of course, you are fee to use any model portfolio on the publication.

Recent blog post for more information on these topics.

If you cannot stomach the volatility of this uncertain

time, you are, of course, free to reduce the aggressiveness of your account by

raising cash or switching to a less aggressive model portfolio. Please see the recent blog post for more information

on this topic. https://marketresilience.blogspot.com/p/changing-portfolio-aggressiveness.html

Reduced Allocations to DJIA-linked ETFs

You may notice that the algorithms for the D5 signal set caused the allocation to the DJIA-linked ETFs (DIA, DDM, UDOW) to decrease this week. The reason driving this shift is that the market has not been responding as the algorithms expected, and the algorithms pull some money out. Basically, they are saying something is going wrong in the markets – take some money out and come back later. We may ultimately conclude that such reduced allocations were not useful in our current situation. But this signal has added value over the last 100 years, and we should follow it.

Following the Disciplines

As you know, I frequently advocate staying with the disciplines. I have seen many professional and non-professional investors lose money and their ability to focus by deviating from their established processes. I was evaluating professional investment managers for pension funds in the 1980s. The 1987 crash was interesting in that many of the investment indicators that investment professionals look at all day about the health of the markets went haywire. The indicators were erratic and in many cases contradictory. When the crash was over, we evaluated what happened and how managers navigated through the conflicting signals.

We found that those who followed their established processes did better. Those who saw the chaos and tried to reconcile all the conflicting indicators did not do as well. They responded to one indicator at one time and another indicator later, and they ended up trading aggressively to conform to what they saw most recently – believing recent information to be most reliable. I say this to disclose my bias in these situations. I feel like we are flying blind in many ways right now. But if we avoid being distracted by trying to reconcile all the conflicting information, I believe that we will navigate this more effectively.

3/22/2020

Research Note: Alphabet of Market Patterns, Valuation - March 22, 2020

Summary of My Near-term Suggestions

The scenario I outline for the recovery can help us make up for losses. In a way that is reliable and prudent. The immediate and pressing task is to determine the right course of action over he next week or two.

Jeff Hansen

Jeffrey.Hansen@me.com

Market Update - March 22, 2020

We are in a purposefully induced cardiac arrest in terms of the economy. While most investors are panicking, let’s keep our wits about us and look for attractive buying opportunities. We can navigate the market through this crisis and make sound investment decisions.

The first part of this note summarizes what I view as the most likely path the market will take from here. The second part has my comment about market context and additional background in the key points. I know some subscribers have adhered to the target weights and others have sold out of their stock ETFs during this decline.

PART ONE

The current MRI conditions suggest that a W-shaped market recovery is most likely. It is also the one that seems to fit the current economic situation and is the one that is most cautious. If we prepare for this pattern, we can easily accommodate other types of recovery pattern, which I discuss below, if they occur.

The diagram below represents the “W” pattern of stock price movements. We have had a dramatic drop in prices that is indicated by the first downleg of the W. We may soon be at the first bottom, which I discuss below in the section on valuation. From there, prices move higher when investors begin to see how some relief from the crisis and/or stocks simply become too cheap to not buy. The peak of the relief rally often coincides with a peak in the Micro MRI and the second decline is often precipitated by negative news that the recovery will be slower than hoped. Based on the current MRI conditions, I believe the second bottom will be easier to identify than the first. Also, I cannot determine right now if the second bottom will be higher or lower than the first.

The yellow box says: "Target weights of current model portfolio, or less aggressive." If at all tolerable, stay with the target weights of the model portfolio

The green box says: "Target weights of current model portfolio, or more aggressive"

Should we find that the W-shaped recovery is not relevant, I will describe what is taking place.

The historical simulation for the main signal set driving the model portfolios (D5) shows it has adapted to the various recovery patterns described in a section below. The graph below shows the simulated D5 performance in the green line. The DJIA as the brown line. The graph is on a log scale. You will note that our approach using a weekly trading discipline did not avoid the crash of 1987 (shown in the green box). But the recovery was reasonable. Over all the approach produced strong simulated returns and avoids many of the major losses over this time period.

Slightly Revised Model Portfolio Lineup on Diamond

The most widely used model portfolios have been Diamond (sg131) and Diamond-Onyx Mix (sg218). I have added model portfolios having the same signal sets and ETFs but are more or less aggressive. Whereas in the past, I discouraged switching model portfolios, the new lineup makes that less of an issue. They are similar enough - varying only by aggressiveness - that moving to an adjacent model portfolio is acceptable.

PART TWO

Market Context

The current situation may be analogous to an intentionally inducted cardiac arrest – shutting businesses to allow people to stay home in order to stop the spread of the virus and to prevent overwhelming the medical system. Leaders around the world have stopped the economy and are at the same time are adding stimulants (checks in the mail, extending unemployment insurance, etc.) to resuscitate the economy. There is often a lag between the time the stimulants are administered and when they take effect, so it is important to apply the stimulants as soon as possible. If we think of the stock markets as the heart rate monitor, we can see that the heart is indeed starting to flatline. We wait anxiously until we see that the economic heart restarts.

Of course, these market dynamics are not entirely explained by cycles of resilience, except to say that the spike in coronavirus cases in the US came when the Micro MRI was in the vulnerable part of its cycle.

I believe a case could be made that if we shut down the economy, we should also shut down the stock markets – the decline in the stock market is making many feel like our economic health is getting worse, when the decline is actually part of the cure that has been prescribed to address this non-economic issue (the virus). We rightfully have understood that the stock market generally reflects the value of the future economic returns of publicly traded companies. When the future appears bleak, stock prices decline. But that may not fit this intentional stoppage and investors hate uncertainty.

I believe the global economy will ultimately be resuscitated, but also anticipate that this episode will bring other underlying problems to the surface, such as too much consumer and business debt. Stock market declines and economic stress typically cause unemployment and push companies out of business, which push stock market prices down further. Some of these suspected non-virus problems could be true and might have produced a recession and market declines on their own over a more extended timeframe. But the virus and this intentionally induced economic arrest bring some of them to the forefront and demand solutions in order to resuscitate the economy.

While the current situation is alarming, I want to stress that what we are seeing is an intentionally induced economic arrest with the stimulus happening almost simultaneously. In past market economic and market declines, leaders have been slow to recognize that economic problems as they are occurring.

In addition to these problems, leaders during the Great Depression of the 1930s came forth with the wrong remedies. They selected a remedy that was a tough love approach. In the time I have today, Wikipedia is my source for this quote, (https://en.wikipedia.org/wiki/Great_Depression):

We fear reliving the Great Depression and the 80% decline in the stock market, and it is probably healthy to keep that experience in mind. But I believe this situation is different. We know that metrics commonly used to indicate recessions and depressions will soon spike. We can expect the unemployment rate to go much higher. Bankruptcies will also increase.

But the key driver of this downturn can end when the virus is contained and the resuscitation steps are already being applied. In recessions developing from within the economy, stimulus packages are typically delayed. Considering the delay and natural lag time required for the stimulus to have an impact, the economy suffers more.

The speed of resuscitation is crucial; the longer it takes, the more the economy deteriorates. Each week, thousands of people will be laid off and companies will slip into bankruptcy. While the coming recession could be deeper than usual because of the synchronized massive global shut down, it could be shorter than usual because of the extraordinary stimulus measures taking place around the world.

The DJIA May Be in the Bargain Basement as of Friday March 20, 2020

We can get an idea of how far prices might drop by looking at Friday’s (3/20/2020) valuation of the companies in the DJIA compared to the lowest levels of prior market declines. The most common valuation measure is the Price-to-Earnings ratio. This relates the current price of the companies to their earnings. However, in the current situation, we may not have a lot of confidence in the any assessment of earnings. The recent past may have little relationship to future earnings given the current economic arrest.

Instead, I’ll focus on the Price-to-Book ratio because it is more conservative. This ratio relates stock price to the hard assets of the company. For example, Apple Computer has buildings, machinery, computers, plants, land, etc. The Price-to-Book ratio looks at the current price relative to those hard assets. This is a conservative measure because it does not consider earnings, which can vary over time. In addition, this ratio does not include intangible assets, such as the brand name, that have real value. Because of the Apple brand and the talent of its people, it is probably worth more than a simple sum of its plants and equipment. Thus, the Apple, Nike, and IBM brands have value that is not considered in the Price-to-Book ratio. To get the average value for the DJIA, the individual company ratios are used to create one ratio for the index.

The two charts below show similar information. The first one provides more context for the points, but I include both because the second because it is easier to read and summarizes the main points. The first chart covers the 1995 to the present, and the DJIA is shown by the dark blue line (not on a log scale) and the Price-to-Book ratio in the thin light blue line. The ratio bounces around, but I’d like to focus on the values at the bottom of major declines. Lower values mean that the price for the stocks is low compared to their hard assets. These values have been similar over the last 25 years and range from a high of 3.5 to a low of 2.3. The current value (as of 3/21/2020) is 2.9. This is down from a ratio of 4.4 just a month ago.

By this measure, prices are closer to the bottom than to the top. So, stock prices are getting cheap. This level may be cheap enough that investors will start coming in simply because they are getting good hard assets at a low price. They may not care what earnings are this year or next year. They simply know that these quality companies are likely going to grow and make good use of these hard assets.

Thus, a week ago (what seems like an eternity), I thought prices could go lower. But now, just because these great companies are moving into the bargain basement, I believe that investors will soon come in and start buying.

The chart below is a simpler version that covers 2000 through the present. It plots the DJIA on a log scale and shows the Price-to-Book ratio for the major market price bottoms. Beginning with the major decline in 2009, the Price-to-Book ratios have been 2.3, 2.3, 2.8, and 3.5. After the market has achieve these levels there has been a strong rebound in prices. The average Price-to-Book ratio over the last four March values (2020, 2019, 2018, and 2017) has been 4.0. Thus, the recent price decline has produced valuation (Price-to-Book ratio) levels similar to recent market bottoms.

Don’t Just Do Something, Stand There

In my training videos, I mention a saying I heard at a conference: Don’t Just Do Something, Stand There. This means that in times of crisis or uncertainty, it is often better to NOT make a change. In general, things are not as bad as they seem. People overreact to their fears sending prices far lower than their true value. The valuation comment above is one reason why this saying is relevant. The MRI status is another reason. The Micro MRI and another important MRI (that I don’t often mention), are both at historic lows. Both suggest that there is more likelihood of prices moving higher than lower. If you can stand the short-term pain of additional big price swings due the crisis atmosphere, the current DJIA level may be a fabulous bargain.

As we have found out, trading one’s account requires that you look at your account balance each week, and the decline in that balance has been painful. With the idea that prices will bounce back, it sometimes helps to think of losses as paper losses – yes, the market has placed a low value on the DJIA at the moment, but the market is not making a sound judgment because of the panic. Investors overreact to both good news and bad news. What we are seeing now could easily be an overreaction that will be ultimately be corrected.

The Alphabet of Market Declines and Recoveries

Unless our economy fails to be resuscitated, there will be a recovery. The question becomes, “What will the recovery look like?” You may hear various descriptions of market recoveries using different letters of the alphabet. The description relates to the letters V, L U and W. At the moment, I believe the W pattern is most likely. This section describes this range of market declines and recoveries.

V-shaped Pattern

A few weeks ago (which seems like an eternity) I urged patience because many sharp declines are "V" shaped. When many investors see a negative event, they panic and sell. When the event passes, the markets recover quickly. Prices decline and make a complete recovery and then continue to move higher. The chart below shows 1974, during the oil shocks of that decade.

L-shaped Pattern

The L-shaped patterns pattern is unusual over the last 100 years. The main example is the 1987 crash and subsequent recovery. The DJIA declined abruptly and sharply over the course of a few weeks. I describe in my material on Focused 15 Investing that a decline of this type cannot be avoided using our weekly trading strategy, and that has proven to be the case in the current market decline. After the decline in 1987, price recovery was slow compared to the V-shaped recovery. It took the DJIA roughly two years to surpass the peak of the market before the crash.

U-shaped Pattern

A U-shaped recovery does not have a sharp rebound but ultimately does rebound. An example of this is the 1990 decline.

It may be most prudent to expect a W-shaped recovery. The decline we have already had is the first down-leg of the W. We should soon approach the bottom of the first decline. Then a rebound indicated by the first upleg of the W. I think it is most prudent to assume it is not going to be a completely recover to the price level of, say, a month ago. The peak in the middle of the W is the end of the relief rally. The second downleg typically comes quickly and the bottom can be higher or lower than the first bottom. The following graph shows the Russian Debt Crisis and Long-term Capital Management collapse in 1998.

If we prepare for the W-shaped recovery, we can easily recognize a shift to a V-shaped one and move forward from there. The shift from W to V can be smooth.

If we prepare for the W-shaped recovery, we can easily recognize a shift to a V-shaped one and move forward from there. The shift from W to V can be smooth.

We should soon find out if the recovery is U-shaped. In this case, declines stop but prices do not move up for a while. After some repair of the economy and greater visibility into the future, prices move higher again.

Please contact me with questions or comments.

The scenario I outline for the recovery can help us make up for losses. In a way that is reliable and prudent. The immediate and pressing task is to determine the right course of action over he next week or two.

- If you have a long-term investment horizon, stay with the target weights of the model portfolio you have selected.

- If you have stayed with the target weights of your model portfolio through the decline, try to stay with them. The valuation analysis I discuss below suggests we may be close to a near-term bottom.

- If the pain gets too much for you, reduce the aggressiveness, which I discuss below.

- If you sold some of your stock ETFs (DIA, DDM, UDOW, XLU, or XLP during the decline, I suggest not making any changes until we are at the near-term bottom of the market, which could occur this week or shortly thereafter. I will send out an alert when I think that is upon us.

- Now is not the time to try to be more aggressive than you have been in the past. There will be a better time for a more aggressive portfolio, which I describe below.

- It is most important to be aggressive later on beginning at the second bottom that appears likely at this time. I will alert subscribers and outline a reasonable course of action.

Jeff Hansen

Jeffrey.Hansen@me.com

Market Update - March 22, 2020

We are in a purposefully induced cardiac arrest in terms of the economy. While most investors are panicking, let’s keep our wits about us and look for attractive buying opportunities. We can navigate the market through this crisis and make sound investment decisions.

The first part of this note summarizes what I view as the most likely path the market will take from here. The second part has my comment about market context and additional background in the key points. I know some subscribers have adhered to the target weights and others have sold out of their stock ETFs during this decline.

PART ONE

The current MRI conditions suggest that a W-shaped market recovery is most likely. It is also the one that seems to fit the current economic situation and is the one that is most cautious. If we prepare for this pattern, we can easily accommodate other types of recovery pattern, which I discuss below, if they occur.

The diagram below represents the “W” pattern of stock price movements. We have had a dramatic drop in prices that is indicated by the first downleg of the W. We may soon be at the first bottom, which I discuss below in the section on valuation. From there, prices move higher when investors begin to see how some relief from the crisis and/or stocks simply become too cheap to not buy. The peak of the relief rally often coincides with a peak in the Micro MRI and the second decline is often precipitated by negative news that the recovery will be slower than hoped. Based on the current MRI conditions, I believe the second bottom will be easier to identify than the first. Also, I cannot determine right now if the second bottom will be higher or lower than the first.

As we get to the first bottom, it will be beneficial for you to have your portfolio match the target weights of the model portfolio you have been following thus far. I know some subscribers have sold stocks because the pain of the losses was great. If you can stomach the uncertainty of the coronavirus economic shutdown, I suggest that when I alert you that the first bottom (i.e., the near-term bottom) is upon us, you get back to the target weights of the model portfolio you have been using. If you are having trouble sleeping at night because of the markets and want to reduce the aggressiveness of your portfolio, you have two options.

You can easily change the aggressiveness of your portfolio by increasing the amount of cash you are holding. You do this on the Shares-to-Trade worksheet by increase the value in Box #2 (cash level). This is the percentage of your account that is not invested in the ETFs listed on the sheet.

Alternatively, you can select a less aggressive model portfolio from the weekly publication.

Please see this page for some additional detail on how to change the aggressiveness of your portfolio: LINK

Historically, the MRI framework has been good at identifying the end of relief rallies, such the end of Upleg A. I plan to give special alert outside of the regular weekly publication that the Micro MRI is beginning to indicate a peak.

At the second bottom, it will be very important to resume following the target weights the model portfolio you are comfortable with longer term, or one that is more aggressive. For example, if you followed Diamond (sg131) during the decline, follow Diamond (sg131) after the second bottom. Or, if you have followed Diamond-Onyx Mix 35-65 (sg218) during the recent decline, follow it after the second bottom.

If you want to be more aggressive after the Second Bottom, consider using Diamond-Onyx 50-50 Mix (sg118). The second bottom might be the most important point over the coming months – fully participating in the rebound of the Second Bottom is very important.

Regarding timeframe, based on the normal cycles of the MRI, I would expect the relief rally to end in May (roughly) and the second bottom to occur in May, June, or July. Of course, these are general estimates and we will get more visibility on the situation as we move forward.

Be ready for special alerts, which I describe in a section below. I anticipate being able to alert subscribers early in the week and you can decide how to respond. I believe we get many benefits from sticking to a weekly trading discipline over the long term. But the current unprecedented situation justifies some flexibility on this.

You can easily change the aggressiveness of your portfolio by increasing the amount of cash you are holding. You do this on the Shares-to-Trade worksheet by increase the value in Box #2 (cash level). This is the percentage of your account that is not invested in the ETFs listed on the sheet.

Alternatively, you can select a less aggressive model portfolio from the weekly publication.

Please see this page for some additional detail on how to change the aggressiveness of your portfolio: LINK

Historically, the MRI framework has been good at identifying the end of relief rallies, such the end of Upleg A. I plan to give special alert outside of the regular weekly publication that the Micro MRI is beginning to indicate a peak.

At the second bottom, it will be very important to resume following the target weights the model portfolio you are comfortable with longer term, or one that is more aggressive. For example, if you followed Diamond (sg131) during the decline, follow Diamond (sg131) after the second bottom. Or, if you have followed Diamond-Onyx Mix 35-65 (sg218) during the recent decline, follow it after the second bottom.

If you want to be more aggressive after the Second Bottom, consider using Diamond-Onyx 50-50 Mix (sg118). The second bottom might be the most important point over the coming months – fully participating in the rebound of the Second Bottom is very important.

Regarding timeframe, based on the normal cycles of the MRI, I would expect the relief rally to end in May (roughly) and the second bottom to occur in May, June, or July. Of course, these are general estimates and we will get more visibility on the situation as we move forward.

Be ready for special alerts, which I describe in a section below. I anticipate being able to alert subscribers early in the week and you can decide how to respond. I believe we get many benefits from sticking to a weekly trading discipline over the long term. But the current unprecedented situation justifies some flexibility on this.

Anticipated Upcoming

Alerts

- Likely First Bottom - At the recent pace of declines, an alert may occur over the next few days. Certainly within a few weeks we will hit the first bottom. Adhere to the target weights of your selected portfolio. The value in Box #2 should be the same or slightly more than what it was on the recent decline. In other words, the aggressiveness of your investment in the stock market should not exceed the aggressiveness of you used during the decline.

- End of First Upleg of the W - If the MRI begin to indicate an inflection point, I will send out an informational alert. I will say in the alert to consider raising the cash level by, say, 20 percentage points. If you typically hold 3%, hold 23% or more. Of course, you may elect to hold more cash and reduce aggressiveness even more.

- Second Bottom – The MRI have successfully identified the situations like the Second Bottom – the Exceptional Macro is specifically designed to indicate this type of inflection point. At that time, make sure you are using the model portfolio you’d like to use over the long term. For those who want to be more aggressive, use the model portfolio to the right of the one you have been using thus far. I will say in the alert to consider reducing cash to your typical minimum, which should be 3-5%.

The yellow box says: "Target weights of current model portfolio, or less aggressive." If at all tolerable, stay with the target weights of the model portfolio

The green box says: "Target weights of current model portfolio, or more aggressive"

Should we find that the W-shaped recovery is not relevant, I will describe what is taking place.

The historical simulation for the main signal set driving the model portfolios (D5) shows it has adapted to the various recovery patterns described in a section below. The graph below shows the simulated D5 performance in the green line. The DJIA as the brown line. The graph is on a log scale. You will note that our approach using a weekly trading discipline did not avoid the crash of 1987 (shown in the green box). But the recovery was reasonable. Over all the approach produced strong simulated returns and avoids many of the major losses over this time period.

The most widely used model portfolios have been Diamond (sg131) and Diamond-Onyx Mix (sg218). I have added model portfolios having the same signal sets and ETFs but are more or less aggressive. Whereas in the past, I discouraged switching model portfolios, the new lineup makes that less of an issue. They are similar enough - varying only by aggressiveness - that moving to an adjacent model portfolio is acceptable.

PART TWO

Market Context

The current situation may be analogous to an intentionally inducted cardiac arrest – shutting businesses to allow people to stay home in order to stop the spread of the virus and to prevent overwhelming the medical system. Leaders around the world have stopped the economy and are at the same time are adding stimulants (checks in the mail, extending unemployment insurance, etc.) to resuscitate the economy. There is often a lag between the time the stimulants are administered and when they take effect, so it is important to apply the stimulants as soon as possible. If we think of the stock markets as the heart rate monitor, we can see that the heart is indeed starting to flatline. We wait anxiously until we see that the economic heart restarts.

Of course, these market dynamics are not entirely explained by cycles of resilience, except to say that the spike in coronavirus cases in the US came when the Micro MRI was in the vulnerable part of its cycle.

I believe a case could be made that if we shut down the economy, we should also shut down the stock markets – the decline in the stock market is making many feel like our economic health is getting worse, when the decline is actually part of the cure that has been prescribed to address this non-economic issue (the virus). We rightfully have understood that the stock market generally reflects the value of the future economic returns of publicly traded companies. When the future appears bleak, stock prices decline. But that may not fit this intentional stoppage and investors hate uncertainty.

I believe the global economy will ultimately be resuscitated, but also anticipate that this episode will bring other underlying problems to the surface, such as too much consumer and business debt. Stock market declines and economic stress typically cause unemployment and push companies out of business, which push stock market prices down further. Some of these suspected non-virus problems could be true and might have produced a recession and market declines on their own over a more extended timeframe. But the virus and this intentionally induced economic arrest bring some of them to the forefront and demand solutions in order to resuscitate the economy.

While the current situation is alarming, I want to stress that what we are seeing is an intentionally induced economic arrest with the stimulus happening almost simultaneously. In past market economic and market declines, leaders have been slow to recognize that economic problems as they are occurring.

In addition to these problems, leaders during the Great Depression of the 1930s came forth with the wrong remedies. They selected a remedy that was a tough love approach. In the time I have today, Wikipedia is my source for this quote, (https://en.wikipedia.org/wiki/Great_Depression):

At the beginning of the Great Depression, most economists

believed in Say's law and

the equilibrating powers of the market, and failed to explain the severity of

the Depression. Outright leave-it-alone liquidationism was

a position mainly held by the Austrian

School.[33] The

liquidationist position was that a depression is good medicine. The idea was

the benefit of a depression was to liquidate failed investments and businesses

that have been made obsolete by technological development to release factors of production (capital

and labor) from unproductive uses so that these could be redeployed in other

sectors of the technologically dynamic economy. They argued that even if

self-adjustment of the economy took mass bankruptcies, then so be it.[33]

Because of the disastrous effects of the tough love approach during the 1930s, today’s remedies that seek to enhance business and personal income continuity. Governments give money to individuals and are backstops for businesses large and small. Thus, indulgent love may sow the seeds of future problems – such as people developing the expectation that if they fail the government will rescue them - but at least the economy can rebound before deep damage is done to the economy as was the case in the 1930s. We fear reliving the Great Depression and the 80% decline in the stock market, and it is probably healthy to keep that experience in mind. But I believe this situation is different. We know that metrics commonly used to indicate recessions and depressions will soon spike. We can expect the unemployment rate to go much higher. Bankruptcies will also increase.

But the key driver of this downturn can end when the virus is contained and the resuscitation steps are already being applied. In recessions developing from within the economy, stimulus packages are typically delayed. Considering the delay and natural lag time required for the stimulus to have an impact, the economy suffers more.

The speed of resuscitation is crucial; the longer it takes, the more the economy deteriorates. Each week, thousands of people will be laid off and companies will slip into bankruptcy. While the coming recession could be deeper than usual because of the synchronized massive global shut down, it could be shorter than usual because of the extraordinary stimulus measures taking place around the world.

The DJIA May Be in the Bargain Basement as of Friday March 20, 2020

We can get an idea of how far prices might drop by looking at Friday’s (3/20/2020) valuation of the companies in the DJIA compared to the lowest levels of prior market declines. The most common valuation measure is the Price-to-Earnings ratio. This relates the current price of the companies to their earnings. However, in the current situation, we may not have a lot of confidence in the any assessment of earnings. The recent past may have little relationship to future earnings given the current economic arrest.

Instead, I’ll focus on the Price-to-Book ratio because it is more conservative. This ratio relates stock price to the hard assets of the company. For example, Apple Computer has buildings, machinery, computers, plants, land, etc. The Price-to-Book ratio looks at the current price relative to those hard assets. This is a conservative measure because it does not consider earnings, which can vary over time. In addition, this ratio does not include intangible assets, such as the brand name, that have real value. Because of the Apple brand and the talent of its people, it is probably worth more than a simple sum of its plants and equipment. Thus, the Apple, Nike, and IBM brands have value that is not considered in the Price-to-Book ratio. To get the average value for the DJIA, the individual company ratios are used to create one ratio for the index.

The two charts below show similar information. The first one provides more context for the points, but I include both because the second because it is easier to read and summarizes the main points. The first chart covers the 1995 to the present, and the DJIA is shown by the dark blue line (not on a log scale) and the Price-to-Book ratio in the thin light blue line. The ratio bounces around, but I’d like to focus on the values at the bottom of major declines. Lower values mean that the price for the stocks is low compared to their hard assets. These values have been similar over the last 25 years and range from a high of 3.5 to a low of 2.3. The current value (as of 3/21/2020) is 2.9. This is down from a ratio of 4.4 just a month ago.

By this measure, prices are closer to the bottom than to the top. So, stock prices are getting cheap. This level may be cheap enough that investors will start coming in simply because they are getting good hard assets at a low price. They may not care what earnings are this year or next year. They simply know that these quality companies are likely going to grow and make good use of these hard assets.

Thus, a week ago (what seems like an eternity), I thought prices could go lower. But now, just because these great companies are moving into the bargain basement, I believe that investors will soon come in and start buying.

The chart below is a simpler version that covers 2000 through the present. It plots the DJIA on a log scale and shows the Price-to-Book ratio for the major market price bottoms. Beginning with the major decline in 2009, the Price-to-Book ratios have been 2.3, 2.3, 2.8, and 3.5. After the market has achieve these levels there has been a strong rebound in prices. The average Price-to-Book ratio over the last four March values (2020, 2019, 2018, and 2017) has been 4.0. Thus, the recent price decline has produced valuation (Price-to-Book ratio) levels similar to recent market bottoms.

It could be that this time is different, but I believe we have declined to a level that might represent the bargain basement for these 30 high quality companies. It may not be wise to reduce aggressiveness dramatically at this time. A slight reduction can be okay if it helps you sleep at night. If you have an investment horizon longer than, say, 7 years, try to stay with the target weights (don’t increase the cash level).

See this link for the companies in the DJIA.

See this link for the companies in the DJIA.

In my training videos, I mention a saying I heard at a conference: Don’t Just Do Something, Stand There. This means that in times of crisis or uncertainty, it is often better to NOT make a change. In general, things are not as bad as they seem. People overreact to their fears sending prices far lower than their true value. The valuation comment above is one reason why this saying is relevant. The MRI status is another reason. The Micro MRI and another important MRI (that I don’t often mention), are both at historic lows. Both suggest that there is more likelihood of prices moving higher than lower. If you can stand the short-term pain of additional big price swings due the crisis atmosphere, the current DJIA level may be a fabulous bargain.

As we have found out, trading one’s account requires that you look at your account balance each week, and the decline in that balance has been painful. With the idea that prices will bounce back, it sometimes helps to think of losses as paper losses – yes, the market has placed a low value on the DJIA at the moment, but the market is not making a sound judgment because of the panic. Investors overreact to both good news and bad news. What we are seeing now could easily be an overreaction that will be ultimately be corrected.

The Alphabet of Market Declines and Recoveries

Unless our economy fails to be resuscitated, there will be a recovery. The question becomes, “What will the recovery look like?” You may hear various descriptions of market recoveries using different letters of the alphabet. The description relates to the letters V, L U and W. At the moment, I believe the W pattern is most likely. This section describes this range of market declines and recoveries.

V-shaped Pattern

A few weeks ago (which seems like an eternity) I urged patience because many sharp declines are "V" shaped. When many investors see a negative event, they panic and sell. When the event passes, the markets recover quickly. Prices decline and make a complete recovery and then continue to move higher. The chart below shows 1974, during the oil shocks of that decade.

The L-shaped patterns pattern is unusual over the last 100 years. The main example is the 1987 crash and subsequent recovery. The DJIA declined abruptly and sharply over the course of a few weeks. I describe in my material on Focused 15 Investing that a decline of this type cannot be avoided using our weekly trading strategy, and that has proven to be the case in the current market decline. After the decline in 1987, price recovery was slow compared to the V-shaped recovery. It took the DJIA roughly two years to surpass the peak of the market before the crash.

U-shaped Pattern

A U-shaped recovery does not have a sharp rebound but ultimately does rebound. An example of this is the 1990 decline.

It may be most prudent to expect a W-shaped recovery. The decline we have already had is the first down-leg of the W. We should soon approach the bottom of the first decline. Then a rebound indicated by the first upleg of the W. I think it is most prudent to assume it is not going to be a completely recover to the price level of, say, a month ago. The peak in the middle of the W is the end of the relief rally. The second downleg typically comes quickly and the bottom can be higher or lower than the first bottom. The following graph shows the Russian Debt Crisis and Long-term Capital Management collapse in 1998.

We should soon find out if the recovery is U-shaped. In this case, declines stop but prices do not move up for a while. After some repair of the economy and greater visibility into the future, prices move higher again.

Please contact me with questions or comments.

3/18/2020

Weekly Note - March 18, 2020

Revised 11:50 am 3/18/2020

The stock market decline has been startling. If you are uncomfortable with the level of aggressiveness of your current model portfolio, I believe it is reasonable to consider shifting near-term to a model portfolio that has a lower maximum exposure to ETFs linked to the DJIA. These ETFs include DIA, DDM, and UDOW. The rest of this note describes changes to the Diamond publication and my communication that will make shifts in aggressiveness easier. Again, these changes affect the Diamond publication. For now, the publications other than Diamond have not changed - please contact me with questions about the other publications.

If you are comfortable with your model portfolio's the level of variability, you need not change.

The stock market decline has been startling. If you are uncomfortable with the level of aggressiveness of your current model portfolio, I believe it is reasonable to consider shifting near-term to a model portfolio that has a lower maximum exposure to ETFs linked to the DJIA. These ETFs include DIA, DDM, and UDOW. The rest of this note describes changes to the Diamond publication and my communication that will make shifts in aggressiveness easier. Again, these changes affect the Diamond publication. For now, the publications other than Diamond have not changed - please contact me with questions about the other publications.

If you are comfortable with your model portfolio's the level of variability, you need not change.

I think everyone is now fully aware of the coronavirus crisis. The economic impact of fighting the virus is

just beginning. The extent and duration of stock price declines, layoffs and

rising unemployment are likely to reverberate through the economy for some

time. I believe the likelihood of a near-term, price rebound has diminished. At

the end of this note, I discuss the current MRI conditions, which drive my

belief that the likelihood of a rapid increase in stock prices (the key reason one

would maintain the current level of aggressiveness) is diminishing.

As economic and market conditions stabilize, we can shift to

model portfolios that have higher maximum exposures to these DJIA-linked ETFs.

We do not want to miss price appreciation when it does occur. I have laid out a framework below for doing

this. The framework has three phases and

makes wider use of the Onyx sleeve of low volatility sectors, which is designed

to do well in challenging market environments, as I describe below.

Three Phases and an Expanded Set of Diamond-Onyx Mixes

Considering recent events and the ambiguity around us, we

need to shift our goals. At this time, they are to be able to sleep at night, to

recoup losses rapidly in a methodical and low risk manner, and to shift

back to a model portfolio that is a good long-term fit when doing so is prudent. Ultimately, we want to take full advantage of the once in a generation investment opportunities that this crisis will present. I see three likely phases over the next

several months:

- High Uncertainty and Market Volatility – We are here now and can expect high uncertainty about the markets’ reaction to the government measures and the real virus situation. Generally speaking, few asset classes are performing as expected. During this phase, I suggest that subscribers who have found the recent losses intolerable consider a model portfolio with lower risk than the one they currently use. One can select a model portfolio to the left (i.e., lower variability) of the one they currently use on the scatter chart provided on the first page of the weekly publication. Patient subscribers with longer investment horizons (say, more than five-years) time horizon can probably stay with their current portfolio. This phase may last a few weeks or more.

- Greater Clarity on the Path the Markets Take – During this phase, I expect the various stock and bond markets to perform more consistent with expectations in terms of magnitude of ups and downs and in relationship to other asset classes. Based on historical precedent, there are two major paths the markets can take after significant declines such as those we have experienced (and may still be experiencing) and formed a bottom: A) the stock market moves higher at a moderate pace for an extended period (as in 1987), or B) the stock market move higher more aggressively (a relief rally) followed by declines in a few months (as in 2008). During this phase, I will alert you when I believe that you should consider having more exposure to the stock market by shifting to a model portfolio to right on the scatter chart.

- Transitioning to the Desired Model Portfolio – One would transition (as needed) to a model portfolio that is a good long-term fit. I suspect this would take place in roughly early summer. Obviously, potentially unknown factors may affect timing.

Because we are now in phase 1, part of our focus is on looking for the time to move to portfolios that have higher allocations to DJIA-linked ETFs. The price declines we are experiencing will ultimately create very attractive opportunities. When the economy and markets settle, prices are very likely to move quite a bit higher than they are now. The MRI provide reliable signals for the long-term market bottoms.

To provide greater flexibility in carrying out the

framework’s phases, I have adjusted the line-up of model portfolios on

the weekly publication. Specifically, I

have added additional Diamond-Onyx Mixes. each has a different maximum

allocation to the D5 signal set using DDM. The D5 signal set was caught off-guard

by the virus but provides very strong signals in many market environments. The Onyx segment (or sleeve) of the model

portfolios rotates among four low volatility sectors that tend to perform well

in bad markets for the DJIA. Onyx rotates among these four sectors based on

their resilience and vulnerability:

1. Consumer staples company stocks in ETF “XLP.” These are food companies, drug stores, and grocery stores. When the economy is bad, people still need food, toothpaste, and toilet paper.