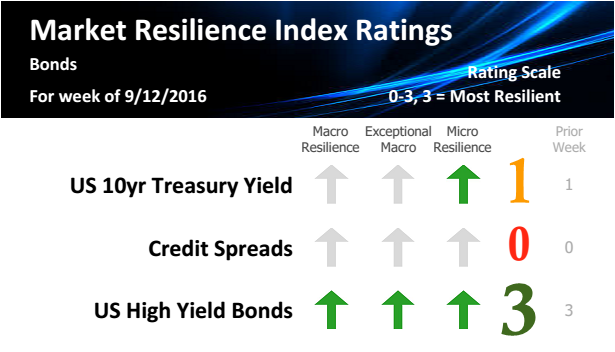

Week of 10/10/2016 – Market Resilience Index Ratings

Both the US stock and bond markets have been

through a period of slightly heightened vulnerability over the last several

weeks. Over the next few weeks, I expect both markets to be able to support

higher prices, with bonds likely to move higher sooner.

This note is a follow-up to the post for the week of 9/19/2016. The table below shows

the Market Resilience Index Ratings for both US 10y bonds and US stocks and

adds the three most recent weeks. The ratings have indicated low resilience

(meaning moderate vulnerability). Compared to earlier periods, the recent price

movements have not been great, but there is some indication that prices have

been affected by the vulnerability. The first table and chart focus on US 10y

bond (I analyze the bond futures TY1 in this case).

Trade Date

|

8/5/2016

|

8/12/2016

|

8/19/2016

|

8/26/2016

|

9/2/2016

|

9/9/2016

|

9/16/2016

|

9/23/2016

|

9/30/2016

|

10/7/2016

|

Bond Market Rating (TY1)

|

2

|

2

|

2

|

2

|

1

|

1

|

1

|

1

|

1

|

1*

|

*

Likely to move to a rating of 2 over next few weeks.

The screen shot below shows the price to TY1 and

two vertical lines. The first line (white) shows when the rating shifted to 2

from 3, effective 7/14/2016. This indicates that high resilience had peaked.

One can see that the prices peaked just before that date. The second vertical

line (red) shows when the rating shifted to 1 from 2, effective 9/2/2016. One

can see that prices softened after that time. The minimum rating is 0, so the

was still some resilience for bond prices. An important point is that from this

point forward, it appears that the rating will increase. Bond prices are likely

to stabilize over the next few weeks and could even move higher.

US stocks, as measured by the Dow Jones

Industrial Average, currently have a rating of 1 and may soon move to a rating

of 2.

Trade Date

|

8/5/2016

|

8/12/2016

|

8/19/2016

|

8/26/2016

|

9/2/2016

|

9/9/2016

|

9/16/2016

|

9/23/2016

|

9/30/2016

|

10/7/2016

|

DJ Industrial Average

|

3

|

3

|

3

|

2

|

2

|

2

|

1

|

1

|

1

|

1*

|

* Likely to move to a rating of 2 over next few weeks.

The chart below shows the recent rating shifts

for the DJIA. The green line shows the shift to 2 from 3, effective 8/16/2016, an

indication that resilience had peaked. This was a good marker of the recent

price action. The yellow line shows the rating shift to 1 from 2, effective

9/16/2016. This appears to be a less meaningful shift in terms of price action.

A key point is that prices have not declined

meaningfully during this period of increased vulnerability, and there are signs

(finer signals than described here) that the period of vulnerability will

dissipate over the next few weeks.

Going forward, I do expect an upgrading of the

resilience of the DJIA. While it has not happened yet, I expect it to take place within a few weeks.

Between now and that shift, we may have some price dips that represent global

stresses, but the duration of the dips is likely to be short given that we see

some modest level of resilience in a number of equity markets globally.

These stock markets are rated 2 (moderately

resilient) or 3 (resilient) for this week: MSCI World, DJ Transports, NASDAQ,

Russell 2000, UK Stocks, Europe Stocks, Emerging Market stocks.

In total, these observations suggest that,

barring major negative news or events, US stock prices can reach new highs over

the next month or so.

Commodities have the highest resilience of the major

asset classes right now.

The S&P Goldman Sachs Commodity Index represents a basket of

commodities, with a high weighting in crude oil. Crude oil (not shown in

graphic) continues to have a rating of 3. Please note that crude is a volatile

asset and can differ meaningfully week to week from the MRI ratings. Over long

periods of time, however, the ratings result in profitable trades.

Gold has a rating of 2, moderately resilient. There may be near-term

price softness, but the Macro and Exceptional Macro MRI continue to be

positive, and prices are likely to be resilient mid-to-longer term.

While much of the world is seeing growing resilience, the situation

for Japan-based investors is different. The USDJPY spot rate is vulnerable to

lower values, which means a stronger yen. This puts downward pressure on the

returns from non-yen investments, such as sovereign bonds excluding Japan

(WGBIxJ) and on the earnings of Japan’s export sensitive stocks (TPX). Both of

these have new ratings of 0 this week.

The DJIA's current rating of 1 (moderate vulnerability) is consistent with the signs of stress found in the strengthening yen and potentially higher bond prices. On balance, however, given the signs of resilience most major equity markets, I believe the stock markets will avoid major declines like those we saw in the summer of 2015 and early 2016, even if the upcoming US election and other political issues may test what resilience is found in these stock markets.