There are important rating changes this week.

Last Friday (9/9/2016) was a big day for the

markets. Concerns about declining bond prices and the potential threats that

rising interest rates pose to global economic growth weighed heavily on the

markets. Both stock and bond markets declined. An added concern was North

Korea’s test of a nuclear weapon. For the week, the DJ Industrial Index

finished -2.2%, and most of that loss occurred on Friday (-2.1%).

Bloomberg News has a good summary (click here) and analyst

comments (here) of the day’s market moves and what might be behind them. The article indicates that the equity market

declined in response to concerns that bond prices are likely to fall from this

point on. Jeffrey Gundlach, a well-respected bond manager, announced on

Thursday that bond prices have peaked and are likely to decline from this time

forward. The logic is that bond prices move lower because of higher interest rates.

As interest rates move higher, stock prices decline because much of the

increase in stock prices over the last several years has been attributed to

extremely low interest rates. If interest rates move higher from here, stocks

will find less support, and both stock and bond prices will fall.

The Market Resilience Index Ratings confirm his

view of the bond market. The table below shows the ratings for the US 10y bond

futures (TY1) and the DJ Industrial Average. The ratings are scaled from 0 to

3, with 0 being the most vulnerable and 3 being the most resilient. The ratings

reflect the number of positive values of three Market Resilience Indexes:

Macro, Exceptional Macro, and Micro.

>>>

Important inflection points occur when a market gains

or loses its Exceptional Macro MRI (see the tab above for an explanation of the MRI ratings). The dates of the loss

of this key MRI are shown by heavy borders.

|

7/15/2016

|

7/22/2016

|

7/29/2016

|

8/5/2016

|

8/12/2016

|

8/19/2016

|

8/26/2016

|

9/2/2016

|

9/9/2016

|

9/16/2016

|

|

Bond Market

Rating (TY1)

|

3

|

2

|

2

|

2

|

2

|

2

|

2

|

1

|

1

|

1

|

|

DJ Industrial Average

|

3

|

3

|

3

|

3

|

3

|

3

|

2

|

2

|

2

|

1

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The MRI ratings for bonds are consistent with Mr.

Gundlach’s assessment. He also states that when rates do rise (and bond prices fall), they will do so

gradually. This too is supported by the MRI levels, at least for the near term. The MRI levels tend to be

cyclical, and the shortest-cycle MRI is the Micro MRI. For bond prices (TY1), the level this week is

low. The current level is lower than 90% of the weekly levels since March 1983. Since it is toward the lower extreme, it is becoming more likely that the Micro MRI will turn positive over the next few weeks. When it does, the rating for the bond market (TY1) will move to 2 from 1,

indicating a higher level of resilience for bond prices. Clearly, Gundlach

makes longer-term forecasts than I am doing here; the Focused 15 Investing approach is responsive to current market conditions as they unfold and does make long term forecasts.

The changes in the MRI ratings for the DJ

Industrial Average have moved more quickly over the recent weeks. The loss of

the Exceptional Macro MRI occurred just this week. This is a important event and one

that we have been watching for over the last several weeks. The loss of this important MRI may last a few weeks or quite a bit longer.

Regardless, we can expect the next few weeks to be a rough ride. The Micro

MRI for the DJIA, which ceased to be positive on 8/26/2016, is at a moderate

level and is likely to move lower. Since 1919, the Micro MRI has been higher in

55% of the weeks and lower in 45%. Thus,

there is still downside to prices and vulnerability on a short-term basis. Without the Exceptional Macro MRI, declines are likely to be more pronounced.

The Focused 15 Investing model portfolios have

been slightly defensive for several weeks and are more defensive this week.

These exposures are driven by the MRI ratings discussed here plus additional MRI-related measures.

The S&P Goldman Sachs Commodity index is now

rated 3, up from 2 the prior week. This move was expected. Commodities have

been beaten down over many months (with little regard to their MRI ratings) and

are have been rebounding. There may be price declines, but declines are not likely to

be dramatic or long lasting given their current ratings. However, commodity prices could move against

their resilience ratings as they did in 2015 given stress in the stock and bond

markets.

Emerging Market stocks also experienced losses

last week. The MRI ratings on this market are more positive. It still has the

important Exceptional Macro MRI, and the Micro MRI is at a high level. Only 5%

of the weeks since 1989 have higher levels, so there may be near-term price

declines and this may add to market stress.

|

7/15/2016

|

7/22/2016

|

7/29/2016

|

8/5/2016

|

8/12/2016

|

8/19/2016

|

8/26/2016

|

9/2/2016

|

9/9/2016

|

9/16/2016

|

MSCI Emerging Market Stocks

|

3

|

3

|

3

|

3

|

3

|

3

|

3

|

2

|

2

|

2

|

At the moment, these declines are likely to be

moderated by the two other positive MRIs that give the rating of 2 (discussed briefly below). Qualitatively,

these markets may be supported by higher commodity prices, as emerging market countries tend to be

commodity exporters. Should a global stress

get very high, emerging markets may move in concert with major markets.

Taking A Step Back

While all this sounds quite pessimistic, the resilience of markets globally

appears stronger at this time than it did in the period March 2015 through

March of 2016. Stock markets in the UK,

Europe and Emerging Markets are all more resilient at this time than in the

earlier period. Unfortunately, Japanese

stocks still appear quite vulnerable.

While these circumstances can change over a period of a few weeks, markets appear able to withstand a moderate level of anxiety about growth at this

time.

And this makes sense. The central banks will raise rates to rise

back to more normal levels as economic growth takes hold.

Additional Asset Class Detail

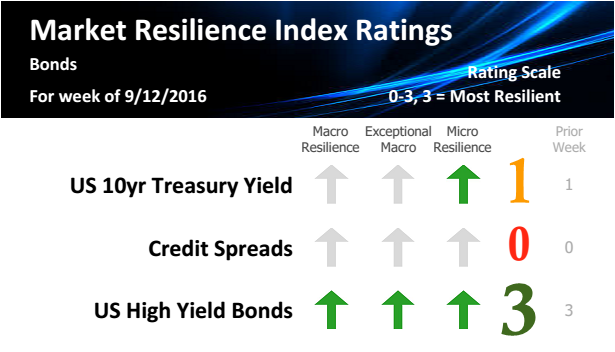

US Bonds

With a rating of 1 on the resilience scale, the US 10y Treasury yield

is moderately vulnerable to declines. I expect this condition to remain in

place for the next few weeks. The Micro Market Resilience Index suggests

resilience, while the Macro and Exceptional Macro continue to suggest

vulnerability.

The US 10y Treasury Futures (TY1) is rated 1,

based on the Macro MRI. It lost the Exceptional Macro MRI for the week of

9/2/2016. I expect the Micro MRI to be present over the next week or so.

US high-yield bonds continue to be rated 3, or highly resilient. All

else being equal, high-yield bond prices will tend to rise. The rating may drop

over the next few weeks to 2, when the Micro MRI ceases to be positive.

Developed Market Stocks

US industrial stocks, as represented by the Dow Jones Industrial

Average, dropped to a rating of 1 this week. It lost the Exceptional Macro MRI

this week, which is a notable shift. While this shift may be temporary, Focused

15 Investing portfolios are more defensive this week.

UK stocks are rated 2 this week, down from 3 as expected.

European stock prices have a rating of 2. At the moment, it appears

that this rating will remain in place for a few weeks.

Commodities

Overall, commodity prices are resilient with a rating of 3, up from 2

last week.

The S&P Goldman Sachs Commodity Index represents a basket of

commodities, with a high weighting in crude oil. Crude oil (not shown in

graphic above) continues to have a rating of 3. Please note that crude is a volatile

asset and can differ meaningfully week to week from its MRI ratings. Over long

periods of time, however, the ratings result in profitable trades.

Gold has a rating of 2, moderately resilient. There may be near-term

price softness, but the Macro and Exceptional Macro MRI continue to be

positive, and prices are likely to be resilient mid-to-longer term.

Emerging Markets

Emerging market stock and bond prices are rated moderately resilient.

At the moment, this appears to be a temporary breather because the Macro and

Exceptional Macro Market Resilience Indexes are both positive.

Chinese stocks, as represented by the Shanghai Composite, have a

rating of 0, which suggests vulnerability to declines.

Currencies

The Dollar index, DXY, is rated 0 and is vulnerable to declines. This

is noteworthy considering concerns about rising rates in the US, which would

typically lead to a stronger USD. We will be watching this conflicting signal.

The Euro is rated 3, but may this rating may be short lived; we may

see a rating of 2 in the next week or so. Regardless, EURUSD may continue to

appreciate because of the positive Macro and Exceptional Macro ratings.

GBP is rated 2, which means it is moderately resilient. This is a new

rating and suggests a positive shift – it was rated 0 just a month ago.