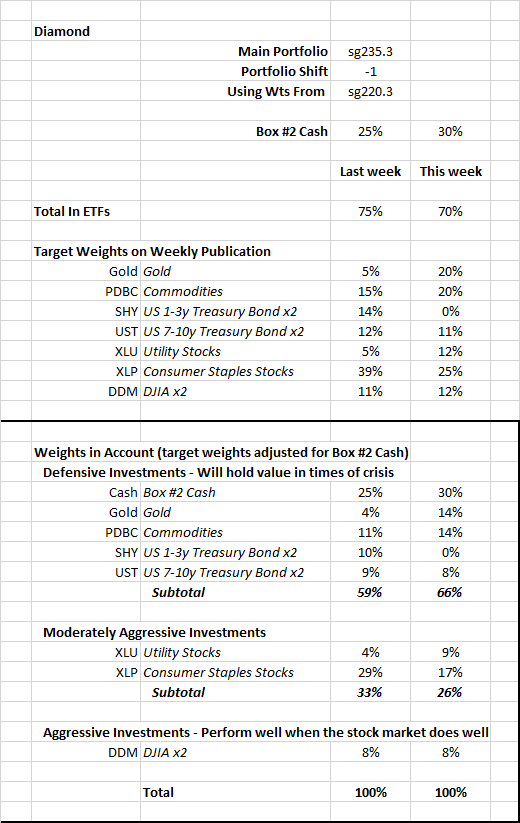

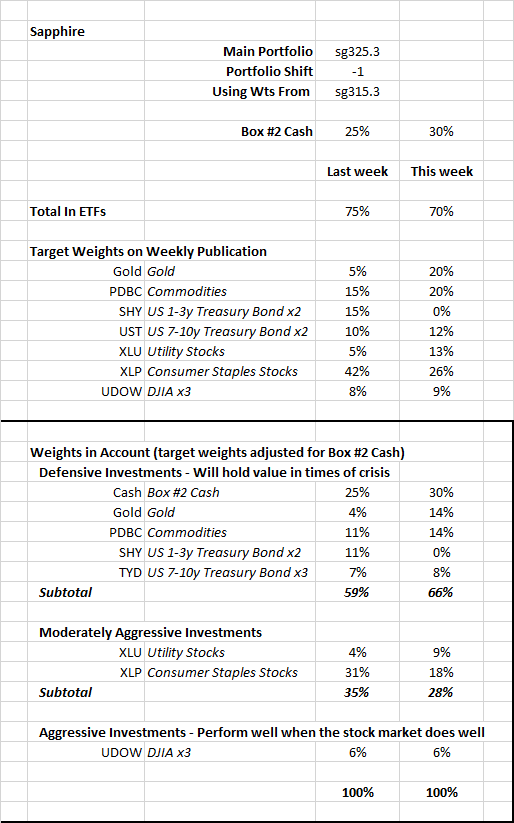

The algorithms call for different weights for the ETFs. The portfolios are positioned for further declines in both the stock and the bond markets.

The upleg in the Micro MRI for the stock market has stalled. Since late December 2021, it has not been making the large swings up and down that we often see; the amplitude of its cycles is muted. I expect this to occur from time to time, and the implication is that declines and gains in the stock market are less extreme. Since 2007, the major stock market declines have occurred during periods when the Micro MRI cycle is NOT muted, which I’ll describe in a future note.

In the section below, I update my comment of last week about, “Higher interest rates may precipitate the end of the counter-trend rally we have seen in stocks over the last few weeks.” In order to get inflation under control, the Fed may have to try extra hard to precipitate meaningful declines in the stock and bond markets.

Update: Higher Interest Rates May Help Precipitate the End of The Counter-Trend Rally

We know that the Fed is concerned about inflation and plans to increase interest rates and to be less supportive of the markets in general. Earlier today, Bill Dudley (president of Federal Reserve Bank of New York from 2009 to 2018 and former vice-chairman of the Federal Open Market Committee) wrote an opinion piece for Bloomberg News with the title: “If Stocks Don’t Fall, the Fed Needs to Force Them.”

Posted below is the opinion piece and a YouTube Bloomberg News interview with Dudley. His main point is that rates will need to go higher in order to reduce inflation. He believes that byproducts of this effort are likely to be more slack in the labor market (a move toward higher unemployment), reduced demand, and tipping the economy into recession.

The MRI have signaled for some time that an economic slowdown is likely. Our portfolios have therefore been defensive for several months. The performance figures show that our portfolios are down a few percentage points since the beginning of the year.

The alternatives listed below (e.g., DJIA, S&P500, VBINX, VASGX) have had larger losses. We are much more defensive than the alternatives listed, which cannot hold cash, so their losses may end up being larger compared to what is possible if the Fed becomes more aggressive in raising rates and reducing the accommodative policies of the last few years.

Performance

The US stock market has declined from December 31, 2021 through last Friday, April, 2022. I have calculated the returns that one would get by following instructions since the beginning of the year for the “main” portfolios for each of the publications. Please see the endnote for a brief comment on the main portfolios.

The year-to-date returns as of 4/1/2022 are:

Diamond: -2.0%

Sapphire: -3.2%

These returns compare favorably to these alternatives:

DJIA: -3.7%

S&P500: -4.3%

NASDAQ: -8.7%

IEF: -7.0% IEF is the ETF for the US 7-10-year Treasury bond index, with no leverage

VBINX: -5.5% VBINX is a Vanguard Fund that has 60% of its assets in stocks and 40% in bonds

VASGX: -5.3% VASGX is a Vanguard Fund that has 80% of its assets in stocks and 20% in bonds

If Stocks Don’t Fall, the Fed Needs to Force Them: Bill Dudley

2022-04-06 10:00:09.17 GMT

By Bill Dudley

(Bloomberg Opinion) -- It’s hard to know how much the U.S.

Federal Reserve will need to do to get inflation under control.

But one thing is certain: To be effective, it’ll have to inflict

more losses on stock and bond investors than it has so far.

Market participants’ heads are already spinning from the

rapid change in the outlook for the Fed’s interest-rate policy.

As recently as a year ago, they expected no rate increases in

2022. Now, they foresee the federal funds rate reaching about

2.5% by the end of this year and peaking at more than 3% in

2023.

Whether that proves right will depend on a number of hard-

to-predict developments. How quickly will inflation come down?

Where will it bottom out as the economy reopens, demand shifts

from services to goods and supply-chain disruptions ease? What

will happen in the labor market, where annual wage inflation is

running at more than 5% and the unemployment rate is on track to

reach its lowest level since the early 1950s within a few

months? Will more people come off the sidelines, boosting the

labor supply? Together with moderating inflation, this could

allow the Fed to stop raising rates at a neutral level of about

2.5%. Or a tightening labor market and stubborn inflation could

force the Fed to be a lot more aggressive.

Among the biggest uncertainties: How will the Fed’s

tightening affect financial conditions, and how will those

conditions affect economic activity? This is central to Fed

Chair Jerome Powell’s thinking about the transmission of

monetary policy. As he put it in his March press conference:

“Policy works through financial conditions. That’s how it

reaches the real economy.”

He’s right. In contrast to many other countries, the U.S.

economy doesn’t respond directly to the level of short-term

interest rates. Most home borrowers aren’t affected, because

they have long-term, fixed-rate mortgages. And, again in

contrast to many other countries, many U.S. households do hold a

significant amount of their wealth in equities. As a result,

they’re sensitive to financial conditions: Equity prices

influence how wealthy they feel, and how willing they are to

spend rather than save.

So far, the Fed’s removal of stimulus hasn’t had much

effect on financial conditions. The S&P 500 index is down only

about 4% from its peak in early January, and still up a lot from

its pre-pandemic level. Similarly, the yield on the 10-year

Treasury note stands at 2.5%, up just 0.75 percentage point from

a year ago and still way below the inflation rate. This is

happening because market participants expect higher short-term

rates to undermine economic growth and force the Fed to reverse

course in 2024 and 2025 — but these very expectations are

preventing the tightening of financial conditions that would

make such an outcome more likely.

Investors should pay closer attention to what Powell has

said: Financial conditions need to tighten. If this doesn’t

happen on its own (which seems unlikely), the Fed will have to

shock markets to achieve the desired response. This would mean

hiking the federal funds rate considerably higher than currently

anticipated. One way or another, to get inflation under control,

the Fed will need to push bond yields higher and stock prices

lower.

To contact the editor responsible for this story:

Mark Whitehouse at mwhitehouse1@bloomberg.net

YouTube Dudley Interview

The Bloomberg interview with Dudley in which he provides additional explanation.

Fed might need to force stocks to fall https://youtu.be/Fiiib9oqTB0

--------------------------

Note – Main Portfolios

The main portfolio in the Diamond publication is sg235. The main portfolio in the Sapphire publication is sg325.

If you use either of these as your long-term portfolio and have followed the instructions since the first of the year by switching to the target weights of a less aggressive portfolio (by adjusting Box #3) and holding Box #2 Cash as instructed, your account’s performance should be close to the figure above.

Some deviation between your account and the numbers above can be expected. The performance figures above assume trading is done at the close of trading on Fridays. Most people trade earlier in the day. In addition, we sometimes trade before Friday. If you use as your long-term portfolio one that is more or less aggressive than the main portfolio, your actual performance will be different.

The figures above are based on the actual ETFs in the model portfolio. The figures in the weekly publication are based on the index that the ETFs track.

Fed might need to force stocks to fall https://youtu.be/Fiiib9oqTB0

--------------------------

Note – Main Portfolios

The main portfolio in the Diamond publication is sg235. The main portfolio in the Sapphire publication is sg325.

If you use either of these as your long-term portfolio and have followed the instructions since the first of the year by switching to the target weights of a less aggressive portfolio (by adjusting Box #3) and holding Box #2 Cash as instructed, your account’s performance should be close to the figure above.

Some deviation between your account and the numbers above can be expected. The performance figures above assume trading is done at the close of trading on Fridays. Most people trade earlier in the day. In addition, we sometimes trade before Friday. If you use as your long-term portfolio one that is more or less aggressive than the main portfolio, your actual performance will be different.

The figures above are based on the actual ETFs in the model portfolio. The figures in the weekly publication are based on the index that the ETFs track.