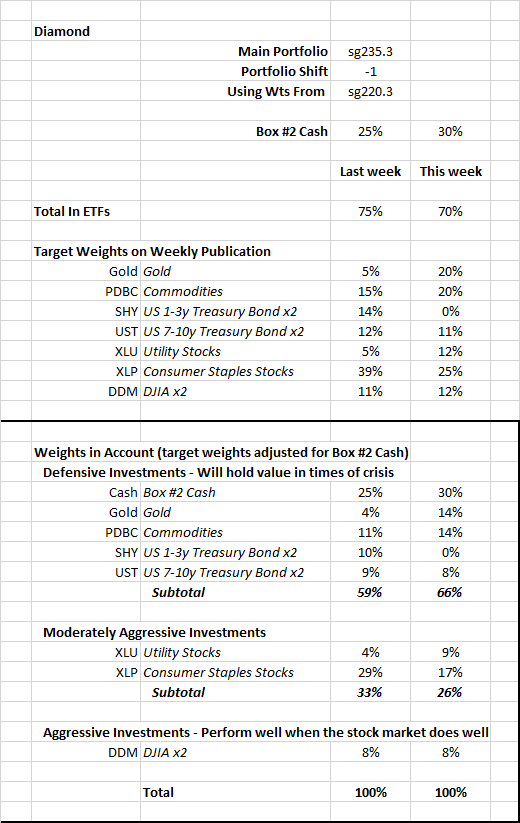

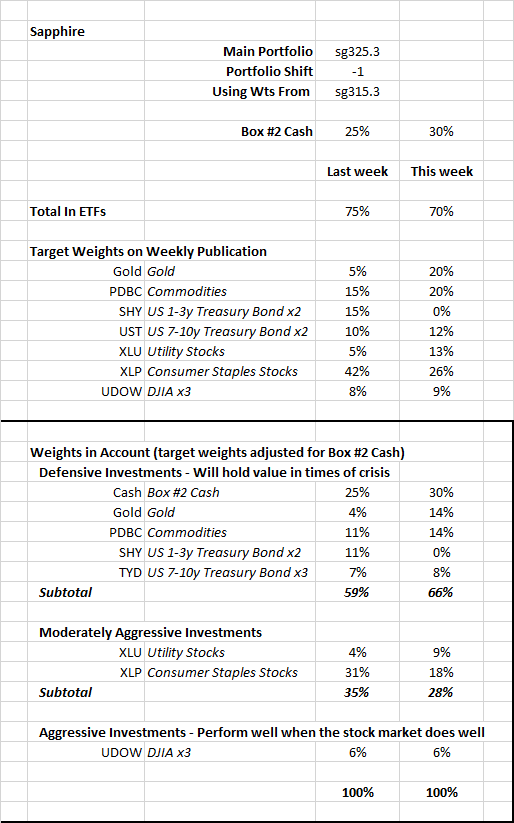

- The performance of accounts that follow the weekly instructions for the main Diamond and Sapphire portfolios since the beginning of the year

- Three themes affecting the markets

- Outlook and Possible Changes in Theme ETFs

1. Performance – Year-to-Date

The US stock market has declined from December 31, 2021 through last Friday, March 4, 2022. I have calculated the returns that one would get by following instructions since the beginning of the year. Specifically, if you followed the “main” portfolio in Diamond (sg235) and switched to alternative target weights and held Box #2 Cash as instructed.

Similarly, if you followed

the “main” portfolio in Sapphire (sg325) and switched to alternative weights,

etc. as instructed. These figures are

based on the actual ETFs in the model portfolios (in contrast, the figures in the weekly publication

are based on the indexes that the ETFs track).

The returns are:

Diamond: -2.6%

Sapphire: -3.2%

If you use as your long-term portfolio one that is more or

less aggressive than the "main" listed in each publication, your actual performance will be different. These returns compare favorably with these

alternatives:

DJIA: -7.2%

S&P500: -8.9%

NASDAQ: -14.8%

VBINX: -7.1%

VBINX (Vanguard Fund that has 60%

of its assets in stocks, 40% in bonds)

VASGX: -8.5%

VASGX (Vanguard Fund that has 80% of its

assets in stocks, 20% in bonds)

The Vanguard funds appear on the Return-to-Variability charts on the first two pages of the weekly pdf. You can see that our portfolios have better return and variability characteristics than the Vanguard funds over the time periods shown.

2. Current Market Themes

Three major themes appear to be affecting the market.

Theme One –

Lower Resilience

From fall 2021 through to the present, the MRI have

indicated decreasing market resilience (greater vulnerability). In the fall of 2021, the computer models and

algorithms reduced aggressiveness of our portfolios, which meant that we moved

out of the stock market. Many of these were false alarms and the

stock market moved higher.

As you may remember, the investment process tends to underperform in

the late stage of an ascending market and there are numerous false alarms just

before a major market decline. This is an apt description of the last months

of 2021. The Macro MRI finally made a clear move to the downleg of its cycle in

mid-December and prices subsequently peaked at the end of December. However, the false alarms suggested that we

were in the late stage of the strong ascending market that would be followed by a meaningful decline.

The research I’ve done on developing longer-term forecasts of market resilience has pointed to lower resilience in the coming weeks as well. The longer-term forecast done in December for the first four months of 2022, called for the Micro MRI for the DJIA to make a double dip, which is for the Micro to form one low point (which occurred at the end of January), move higher, and then return to form another low point before moving toward its normal high level. This happens from time to time and it is happening now, as forecasted in December. The Micro MRI is now in the downleg of a cycle. Unfortunately, this downleg is occurring when there is high inflation, a war in Europe, supplies of commodities are being reduced because of the war, the Fed is poised in raise interest rates, and the Macro MRI is clearly in the downleg of its cycle.

Since mid-December, the market has moved generally in accordance with the forecasted resilience levels. If that continues to be true, we can expect additional

stock price vulnerability and possibly price declines over the next few weeks.

In addition, some valuation measures (price-to-sales, price-to-book ratios) suggested that late 2021 might be a period of

peak company earnings; the market may have been anticipating a decline in

earnings. Thus, both the MRI and the valuation measures suggested future economic

weakness.

The forces in this theme are not part of the computer models or algorithms but they do affect my decisions about Plant/Wait/Harvest designations, the inclusion of theme-related ETFs (such as the current commodity and gold ETFs we currently hold), and Box #2 cash levels.

Theme Two – High

Inflation

The prevailing narrative during late 2021 was that inflation

would be high going forward and the Fed would be forced to increase interest

rates. Inflation was moving higher because of Covid recovery spending and very low

interest rates. Commodity prices were indeed

moving higher. The major commodity index

(S&P Goldman Sachs Commodity Index) peaked in price in October of 2021 and

was somewhat lower at the end of the year, which was consistent with slower

economic growth discussed in theme one.

There was much discussion of when and by how much the Fed

would increase rates. Increasing interest

rates would tend to make investors more concerned about the high stock valuation

measures that had developed during the Covid stimulus spending and abnormally low rates. The

NASDAQ index, which is biased toward growth stocks with high valuations, peaked at the

end of November and has had the biggest year-to-date decline mentioned above.

While stocks can well during periods of high inflation and interest rates over the long term, over the short term, prices often drop in order to achieve valuation levels better suited to higher interest rates.

Theme Three –

Economic Upheaval Related to Russian Invasion

This theme is new. The

Russian invasion of Ukraine has resulted in higher oil and grain prices. The commodity ETF “PDBC” has increased by a startling

10.7% in the two weeks since its inclusion (February 18) through today. That figure includes today’s (March 9, 2022) sharp

decline. While the price of oil is

volatile and we can expect sharp moves (both positive and negative), the 10.7% figure is a very sharp move

up in only two weeks.

From Barrons: “Russia is the third-largest producer of

petroleum after the U.S. and Saudi Arabia, exporting almost 5 million barrels a day of

crude oil in 2020, according to the U.S. Energy Information Administration.

Almost half of those exports went to European countries, while 42% went to Asia

and Oceania.”

(https://www.barrons.com/articles/russia-oil-imports-ban-crude-prices-51646667317)

In addition, Russia and Ukraine supply 30% of the world’s major

grains.

From Time magazine: “Russia and Ukraine together supply nearly a third of the world's wheat and barley exports, which have soared in price since the invasion. The products

they send are made into bread, noodles and animal feed around the world.

All else equal, higher commodity prices can reduce demand. This is especially true when energy prices

move higher. People drive less, turn

down their thermostats, and companies find alternatives to oil. In addition, higher commodity prices in general increase inflation readings and therefore encourage the Fed to increase

rates. But, considering that we have

open battles in Europe, the Fed is, I believe, less likely to raise rates aggressively out

of concerns for helping to tip the country into recession during a time of war.

One scenario is that the Fed raises rates only slightly and allows

economic growth and inflation to be higher than they otherwise would be. Others include increasing rates and helping

to tip the economy into recession.

3. Outlook and Possible Changes

My current concern in this quickly evolving situation is

that theme one – the inherently low resilience of the coming weeks - is not

widely recognized. Low resilience means

that when there is bad news the market goes down and stays down; it doesn’t recover

quickly or completely. We may have

tipped into a mild recession anyway without theme three (Ukraine). The price movements of the major stock

indexes so far this year generally support the validity of this concern. In addition, themes two and three seem able to

provide several opportunities for bad news to occur. In many past crises, the main event (in this case war in Ukraine) produces follow-on events over the subsequent weeks and months that are themselves bad news for stocks.

I am therefore increasing the Box #2 Cash to 35%. As mentioned last week, we may see a counter-trend rally over the next week or so, but I believe that it will be fleeting if it does occur.

Also, the level of Box #2 Cash has remained high since the beginning of the year. The Plant designation lasted just one week (the beginning of February), but an expected countertrend rally failed to materialize. I anticipate reducing this cash level during the next Plant season.

I can envision scenarios that would result in us selling the

commodity and gold ETFs. Should we need sell out of them outside the regular

Friday trading schedule (most likely on a Tuesday), then I will alert you by email.

In addition, I am considering:

- A different ETF for the commodity exposure – one that has less weight in energy and more in agricultural commodities

- Including the clean energy ETF that we used in the Emerald portfolio, which is starting to move higher after being down for several months. Low carbon energy companies may get a boost in the current situation.

- Including an ETF for aerospace and defense companies. Regardless of what happens in Ukraine, there will be more spending on defense in the US, Europe, and Asia.

End