- Increase SHY by about 23% pts. SHY is the most cash-like bond ETF we hold

- Increase gold ETF GLD by about 5% pts

- Increase our 10-year bond ETFs (UST or TYD) by about 3% pts

1. My thoughts about the safety of accounts at Schwab

2. Current valuation of the DJIA suggests the downward pressure on stock prices is not over

3. A key driver of Micro MRI indicates more vulnerability to come

1. The Safety of Our Accounts at Schwab

- I believe my accounts at Charles Schwab brokerage are safe.

- It is important to differentiate between the stock of Schwab the company and the safety of investment accounts held within the Schwab’s brokerage arm.

- The stock for the Charles Schwab Company (Ticker SCHW) has dropped in recent days, which has been widely reported in the news. As of this writing (Monday 3/15/2023) it has dropped about 30% from its recent high on January 10, 2023.

- A decline in the price of Schwab company stock does not mean investment accounts are less secure. It does suggest that Schwab the company may have lower profits going forward because higher interest rates have affected the company’s own assets (some of which are held as bonds).

- Investment accounts are held in the account holder’s name at the brokerage within Schwab and cannot be accessed or used by the Schwab company.

- Investment accounts held at major brokers, including Schwab, are insured by the Securities Investor Protection Corporation (SIPC) for amounts up to $500,000 for securities (e.g., ETFs) and $250,000 in cash.

- In addition to this insurance, Schwab has a third-party insurer as a back-up measure for the investment accounts. I was told this by phone on March 13. Schwab does not disclose the name of the insurer.

- Schwab has a web page devoted to recent events (note 1).

- The webpage states they have been receiving inflows from clients – including on Thursday and Friday of last week. “Our growth and momentum have continued in March, with daily net new assets of over $2 billion per trading day month-to-date, including Thursday and Friday of last week.”

- This would be the opposite of a run on their assets.

- The investment publication Barron’s published an opinion that the recent decline of the Schwab company stock may make the stock an attractive purchase (note 2). This would be the opposite of what has occurred at SVB and other regional banks. An attractive stock price for the Schwab company is not relevant to us because we do not buy individual stocks; we buy ETFs. It does, however, indicate that the stock of Schwab the company may be poised for a rebound after the current anxiety has passed.

2. Valuation and the Actions of the Fed Continue to Weigh on Stock Prices

Focusing just on valuations, the valuations ratios of Price-to-Sales and Price-to-Book for the DJIA (based on a weighted average of all ~30 companies in the index) are both currently at the 85th percentile of levels since 2000. These high levels suggest the DJIA is still expensive and, all else equal, likely to decline.

3. A Key Driver of Micro Market Resilience Index

The Macro MRI, which measures the longest cycle of resilience is not clearly in either the upleg or downleg of its cycle; it is currently moving horizontally, which unusual. Thus, the longer-term trend of the market is not clear at this time.

Over the last few years, we have identified what we believe to be important drivers of investor optimism and pessimism. These are unrelated to the current market environment but give an early indication of how optimistic or pessimistic investors will be over the coming weeks. They therefore foreshadow how the MRI might move.

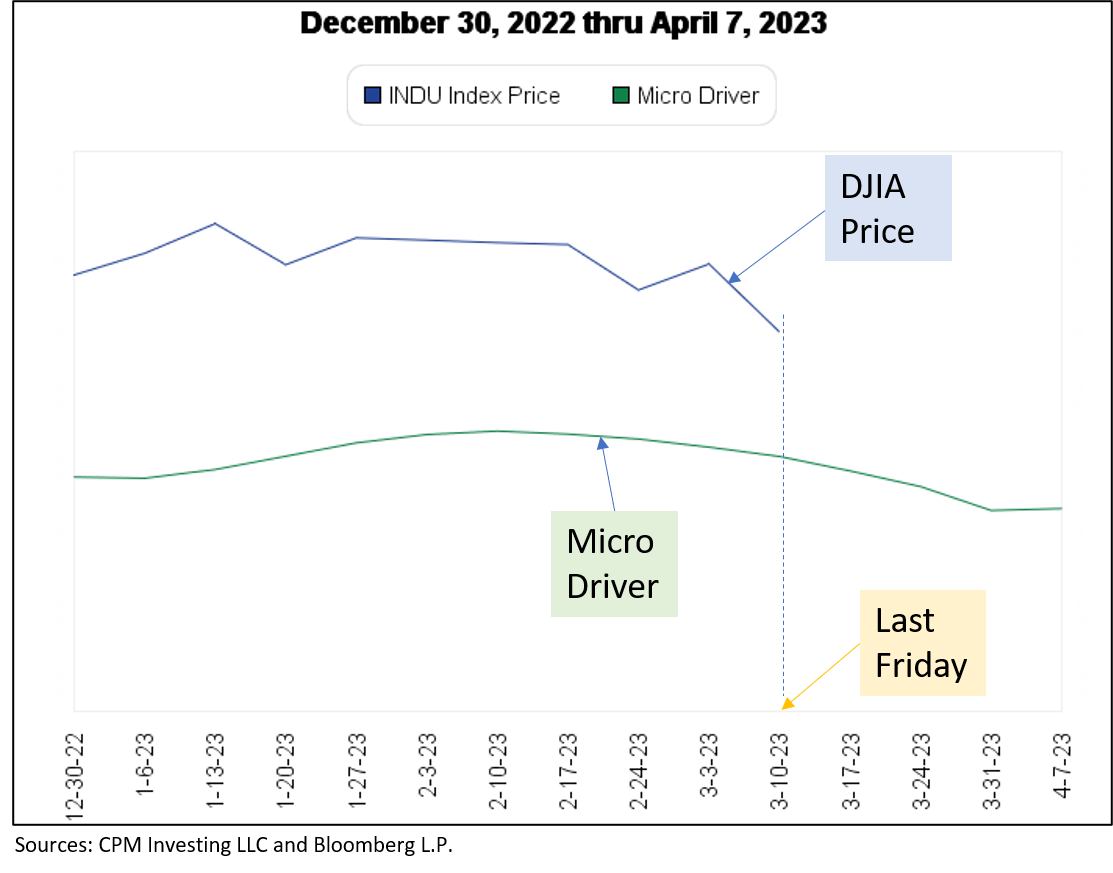

Figure 1 below shows the price of the DJIA (log scale, blue line) and the driver for the Micro MRI, labelled “Micro Driver” (green). The most recent date, March 10, 2023, is shown as a dotted vertical line. The time period covers December 30, 2022 through April 7, 2023 on the horizontal axis. The vertical scale is not shown because our focus is on the relative changes of these lines over time. The actual MRI are not shown.

As you can see, the DJIA has generally followed the Micro Driver over the last several weeks. If this continues, the DJIA will remain vulnerable to declines into April. Since the Macro MRI is moving horizontally (as mentioned above), it is not likely to contribute to higher levels of market resilience over the coming weeks. This means that any bad economic and financial news are more likely to negatively affect stock prices. This view is supported by the driver of the Macro (not shown), which has been moving horizontally for several months.

Thus, our portfolios have been defensive, and are likely to remain defensive until the Micro and/or Macro MRI cycles turn to the uplegs of their cycles. Based on the trajectory of the Micro Driver in Figure 1, it looks like an upleg in the Micro MRI will be at least two weeks away. Accordingly, the next Plant season is a few weeks away.

------------------------------------------------

Notes

1. Schwab Website

Quote from Schwab Company website https://www.aboutschwab.com/perspective-on-recent-industry-events.

Extracted March 13, 2023.

· “We believe one of the best indicators of the strength and stability of the firm is our client activity. Our February results show that clients entrusted Schwab with more than $41.7 billion in net new assets – our second-strongest February ever following our strongest January ever. Our growth and momentum have continued in March, with daily net new assets of over $2 billion per trading day month-to-date, including Thursday and Friday of last week.

· Following the recent events in the banking industry, we are pleased to see the U.S. Treasury Department, Federal Reserve, and FDIC step in with decisive action to support depositors during this critical time. We think the steps announced today provide an additional layer of protection for individuals and will help boost confidence in the American banking system.

· Collectively, more than 80% of client cash held at Schwab Bank is insured dollar-for-dollar by the FDIC. According to S&P Global Market Intelligence, that percentage is among the highest of the top 100 U.S. banks. As a comparison, the banks in the news the last few days have between 2% and 20% of their deposits insured.

· As a further safeguard, Schwab has access to over $80 billion in borrowing capacity with the Federal Home Loan Bank (FHLB), which is an amount greater than all our uninsured deposits. That helps provide the firm significant access to liquidity, so money is there when clients need it.

· Investments at Schwab are held in investors’ names at the Broker Dealer. Those are separate and not comingled with assets at Schwab’s Bank.”

2. Barron’s Article on Schwab Company

Stock

Quote from Barron’s article https://www.barrons.com/articles/charles-schwab-stock-price-bank-selloff-4bb1ae5f). Extracted march 13, 2023.

“Many banks and companies with

related banking entities, such as Charles Schwab, also have a material amount

of fixed income securities on their balance sheet with unrealized losses, as

recently rising interest rates have decreased the value of fixed income

securities,” Morningstar analyst

Michael Wong wrote in a March 9 research note. He said he wasn’t concerned

about Schwab’s liquidity or capital levels and doesn’t plan to change his $87

fair-value estimate. He says shares are undervalued.

Wong notes that Schwab had $36.6

billion of shareholders’ equity and a Tier 1 leverage ratio (a measure of core

capital to total assets) of 7.2% at the end of 2022. That’s above the company’s

internal target, and the regulatory minimum is 4%, Wong writes.

Buying opportunity? Analysts

Richard Repetto and Patrick Moley at investment bank Piper Sandler were quick

to note the differences between Schwab and SVB, writing in a March 10 research

report that “yesterday’s sell off is overdone and could present an attractive

entry point into one of the strongest brands in financial services.”