- pricing for a recession (supports higher Treasury bond prices, all else equal)

- pricing for inflation (weaken support for bonds and DJIA stocks short term, supports higher commodity prices and growth stocks)

- pricing for stronger economic growth (supports higher stock prices)

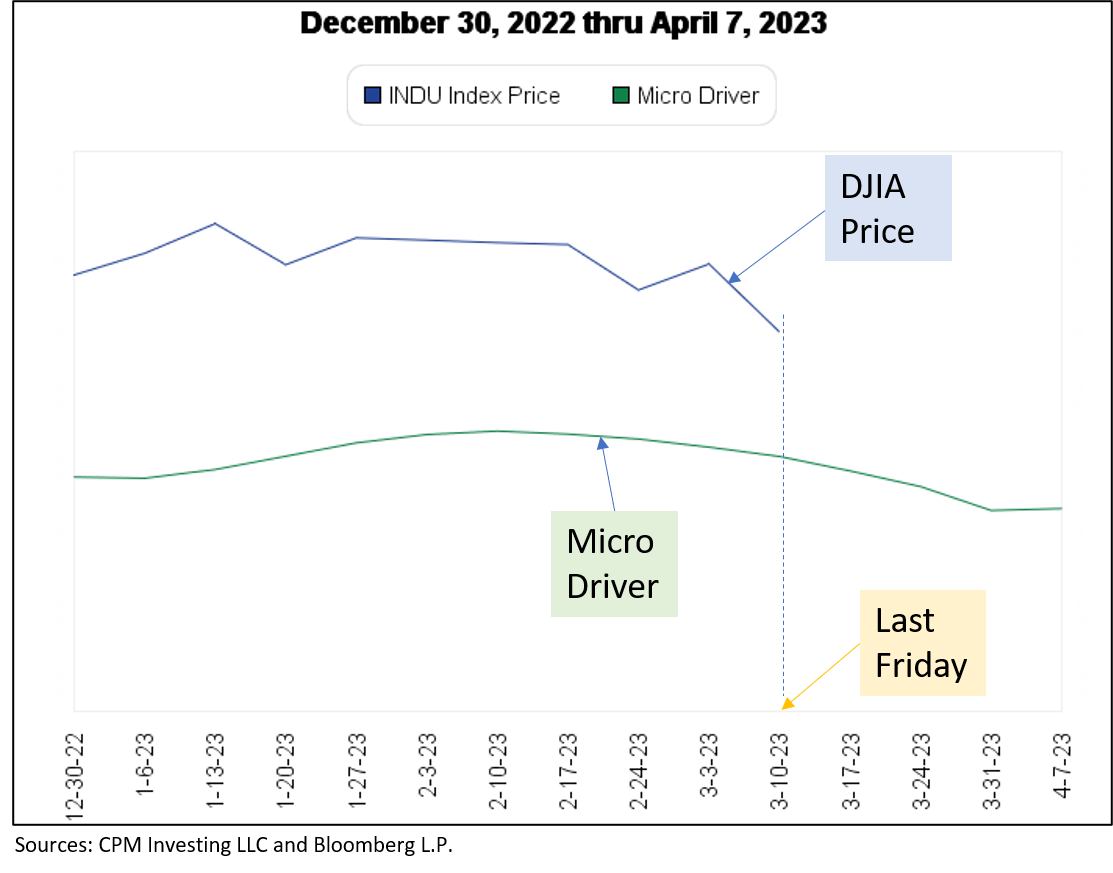

The MRI for the DJIA indicate that while longer-term (Macro) resilience continues to be present, it is fading. The short-term (Micro) resilience cycle is in its downleg but has far to go before reaching the bottom of that cycle; it is at the 60th percentile of levels since 1918. The Exceptional Macro, which could compensate for the Micro MRI being in its downleg, is no longer present. This mix suggests a moderately high level of vulnerability for DJIA prices. The algorithms continue to have low target weights for stocks.

Some of the recent changes in the MRI might be related to the debt ceiling negotiations in Washington. The strength of the longer-term (Macro) resilience was not high prior to the negotiations possibly due to existing concerns about an impending recession and high stock valuations. The debates may have added to those concerns. The drivers of resilience that we recently developed suggest that stock market resilience should be stronger than it has been recently, which supports the idea that stock market investors are becoming more concerned about these issues.

If recession does indeed become the dominant issue, our bond investments can provide a good source of return in our portfolios.

Should the market start pricing for stronger economic growth and lower inflation, our current stock and bond investments can perform well. The MRI have recently suggested that this was a plausible scenario. Support for this path can be seen in the low unemployment rate and lower recent inflation readings.

Should the market start pricing for stronger growth and persistently high inflation, we will need to resume investments in a commodities ETF. I discuss the addition of a different commodities ETF in the section below. The upcoming addition of ETF COM is intended to address the long-recognized shortcomings of many of the dominant commodities ETFs.

During a period of stronger growth and persistently high inflation, portfolio performance will also be helped by the addition of a NASDAQ-linked ETF to gain greater exposure to the stocks of higher growth companies. A NASDAQ-linked ETF has not been included in our portfolios thus far because of the tendency during the early 2000s for high growth companies to experience bubble conditions that are difficult to navigate using the MRI. However, our algorithms navigated the recent decline in the NASDAQ well and NASDAQ-linked ETFs will be a good complement to our DJIA-linked ETFs. We do not envision the NASDAQ ETFs replacing the DJIA ETFs.

The portfolios currently hold a high number of ETFs to provide exposure to different asset classes but this is temporary. A lower number makes trading easier. To address this issue, I have indicated that BITO and SHY (cash-like bonds) are optional holdings. If you find it difficult to trade the current portfolio, you can simply not own these and hold that money as cash in your account.

NASDAQ-Linked ETFs

We will be adding NASDAQ-linked ETFs to the portfolios in the coming weeks but are likely to start at a very low weight. Our signals indicated that early April 2023 was a good time to buy the NASDAQ-linked ETFs. Unfortunately, we did not respond by adding NASDAQ at that time and have missed the strong returns since then. To date, this has been a mistake. While NASDAQ is a good long-term addition to the portfolios, this may not be a good time to give it a meaningful weight in the portfolio because its Micro MRI is currently very high in its cycle. Thus, it will likely have a small weight in the portfolios until a better buying opportunity occurs. Figure 1 below shows DJIA and NASDAQ performance for the recent twelve months.

Figure 1

Figure 2 below shows how our algorithms have timed exposure to NASDAQ. Figure 2 shows a 2x leveraged ETF (QLD) if bought and held over time (red line, labelled “Policy Weights”) and if bought and sold to avoid losses (gold line, which is called the traded sleeve) with the money invested in bonds when not in QLD.

Figure 2

In the early 2000s, the losses of the traded sleeve (gold) are less than simply holding the ETF (red), but were still too high for the ETF to be a good addition to our portfolios.

However, the traded sleeve (gold) avoided the worst losses since 2021 and indicates that our algorithms work effectively. Their greater effectiveness may be primarily the result of the maturing of the companies in the index - the NASDAQ of today is different than the NASDAQ of the early 2000s. The largest holdings of the NASDAQ ETFs are currently Microsoft, Apple, NVIDIA, Amazon, and Google – clearly major companies. While I do not have access to the names of the companies representing the largest holdings in 2000, the major companies of NASDAQ did not have the similar global stature and existing businesses of those dominating NASDAQ today.

A figure showing trades for the ETF QQQ (no leverage) and TQQQ (3x leverage) would show a similar pattern relative to holding the respective ETFs long term without trading.

Adding ETF COM for Commodities Exposure

An investment in commodities can provide positive returns during inflationary periods. I have been following commodities since the mid-2000s and the track record of the algorithms since that time has been good relative to the main commodities index, which is tracked by the ETF GSG. Figure 3 below shows the commodities ETF GSG without trading to avoid losses (red line, labelled “Policy Weights”). It also shows the return of using our algorithms to avoid losses (gold line, labelled “Sleeve”). I started running these signals in real life at the time indicated by vertical green line (July 2008).

Figure 3

The traded sleeve (gold) has far better performance than holding GSG long term (red). Yet, the performance of the traded sleeve (gold) is still too volatile for our purposes. The losses in 2020 and 2022 were dramatic.

A long-standing problem with most commodity ETFs (including GSG and PBDC, both of which we have used) is that they are heavily biased toward energy commodities (such as oil and gas). They currently hold about 60% of their assets in energy commodities. Energy commodities have had a large impact on inflation so this makes sense. But in general, we avoid investing in assets that are heavily influenced by the decisions of small group of people. Energy prices have been heavily influenced by OPEC decisions and government policy. This aspect of the major commodity ETFs plus the normal volatility of energy prices has always made commodities an uncomfortable addition to our portfolios.

Furthermore, there are commodities other than oil and gas that perform well during times of inflation, such as industrial metals (e.g., copper and aluminum), precious metals (gold and silver), and agricultural (wheat, cattle). Gold can be an important commodity in times of stress so we have used a gold ETF to get the needed exposure.

The ETF COM is different than SGS and PDBC. It does not hold static exposures to commodities. Instead, it tracks a rules-based index that began in October of 2010 that invests in a range of commodities. When a commodity exhibits a positive price trend for a specified period of time, the index increases the weight of that commodity. It will invest in up to 12 commodities (through futures contracts). The index has a simulated track record prior to 2010, which we have evaluated.

Figure 4 below shows three commodity ETFs, GSG (one of the largest and oldest), PDBC (which we have used most recently), and COM (which we plan on adding). The time period is May 2015 (the inception of PDBC) through May 31, 2023.

Figure 3

The traded sleeve (gold) has far better performance than holding GSG long term (red). Yet, the performance of the traded sleeve (gold) is still too volatile for our purposes. The losses in 2020 and 2022 were dramatic.

A long-standing problem with most commodity ETFs (including GSG and PBDC, both of which we have used) is that they are heavily biased toward energy commodities (such as oil and gas). They currently hold about 60% of their assets in energy commodities. Energy commodities have had a large impact on inflation so this makes sense. But in general, we avoid investing in assets that are heavily influenced by the decisions of small group of people. Energy prices have been heavily influenced by OPEC decisions and government policy. This aspect of the major commodity ETFs plus the normal volatility of energy prices has always made commodities an uncomfortable addition to our portfolios.

Furthermore, there are commodities other than oil and gas that perform well during times of inflation, such as industrial metals (e.g., copper and aluminum), precious metals (gold and silver), and agricultural (wheat, cattle). Gold can be an important commodity in times of stress so we have used a gold ETF to get the needed exposure.

The ETF COM is different than SGS and PDBC. It does not hold static exposures to commodities. Instead, it tracks a rules-based index that began in October of 2010 that invests in a range of commodities. When a commodity exhibits a positive price trend for a specified period of time, the index increases the weight of that commodity. It will invest in up to 12 commodities (through futures contracts). The index has a simulated track record prior to 2010, which we have evaluated.

Figure 4 below shows three commodity ETFs, GSG (one of the largest and oldest), PDBC (which we have used most recently), and COM (which we plan on adding). The time period is May 2015 (the inception of PDBC) through May 31, 2023.

Figure 4

All three ETFs provided exposure to commodities during the sharp move higher (blue arrow) beginning in 2020 and ending in early 2022, which is a good characteristic for our portfolios. But COM (black) does not have the sharp declines seen in the other ETFs, which is an added benefit.

In our evaluation of COM, we found our long-term (Macro) MRI has done a good job of smoothing out the returns even further. Figure 5 below shows the performance of COM (red), and trading using the models we developed for it (gold line). This analysis was done recently so is not as objective as that shown for the GSG in Figure 3, but the figure below does suggest that COM has a regular cycle of resilience that we can use to smooth returns.

All three ETFs provided exposure to commodities during the sharp move higher (blue arrow) beginning in 2020 and ending in early 2022, which is a good characteristic for our portfolios. But COM (black) does not have the sharp declines seen in the other ETFs, which is an added benefit.

In our evaluation of COM, we found our long-term (Macro) MRI has done a good job of smoothing out the returns even further. Figure 5 below shows the performance of COM (red), and trading using the models we developed for it (gold line). This analysis was done recently so is not as objective as that shown for the GSG in Figure 3, but the figure below does suggest that COM has a regular cycle of resilience that we can use to smooth returns.

Figure 5

During the long period in which there were small positive returns (2011 through 2016) we would not have a meaningful target weight for ETF COM. We plan on using it tactically when positive returns are expected. Our current reading for COM is to have a target weight of zero but that positive returns may develop in the foreseeable future. Thus, adding this ETF over the next few weeks makes sense.

-----------