Summary

The current MRI dynamics of the DJIA and the US Treasury bond indexes suggest that both stocks and bonds will move higher from here. Over the next few weeks, we are likely to see greater resilience emanating from natural sources as indicated by the drivers mentioned below. That said, the current weakness of the Exceptional Macro for the DJIA, high stock valuations, and the upcoming period of high investor excitability beginning in early June (at the latest) are the main focus of our attention for the coming several weeks.

Note: For the next several weeks, we will be holding more ETFs than usual. Over the next month or two, we will identify redundant ETFs and remove them to make trading easier. The research on the drivers has resulted in lower trading, which has made a higher number of ETFs in the portfolios more acceptable for the time being.

Please see this page for descriptions of the language used to discuss our Market Resilience Indexes® https://focused15investing.com/language

Since the end of 2021, the stock and bond markets have faced significant challenges. These include a persistent war, inflationary pressures, central bank actions to combat inflation by raising interest rates, and concerns about a possible recession caused by higher interest rates. The Federal Funds rate increased to 4.83% from a low of 0.06% in June of 2021.

Despite these challenges, the decline in the DJIA has been minimal, declining only 1% since the beginning of January 2021 through last Friday (April 7). Plus, stock valuations have remained high for the last 18 months (see this page for current valuation levels: https://marketresilience.blogspot.com/p/djia-historical-valuation-comparison.html. Many market commentators have wondered why stock investors have not sold their stocks in a panic similar to those seen in March 2020 (Covid) and 2008 (Global Financial Crisis).

From our perspective, the answer may lie in the physics-based drivers of resilience that give rise to the market fluctuations we track with the MRI. At the end of 2021, we determined that the next 12 to 18 months would be a period of low investor excitability. Market gains and losses are muted during such periods. The declines of 2008 and 2020 occurred during periods of high investor excitability, as did most of the major stock market gains and losses of the last 100 years.

The current low level of investor excitability has, we believe, resulted in the absence of significant declines in stock prices over the last 15 months. However, we anticipate that this period of low investor excitability will come to an end by the end of May, based on objective non-market drivers of investor risk aversion. After that time, we are more likely to see investor euphoria and panic and larger price swings higher or lower.

Unfortunately, it is unclear at this time whether the dramatic moves will be higher or lower. Investors may attempt to correct the currently high stock valuations by selling stocks and driving down their prices. Or they may favor stocks due to the expectation of lower future interest rates and a positive trajectory for both stocks and bonds. Based on our analysis of current conditions, the expected shift is currently toward greater in investor risk tolerance and market resilience.

The sections below show the current MRI conditions of key stock and bond markets, which will show the generally positive trajectory for both stocks and bonds. We update our view of conditions each week and will respond as needed.

The DJIA Over the Last 15 Months

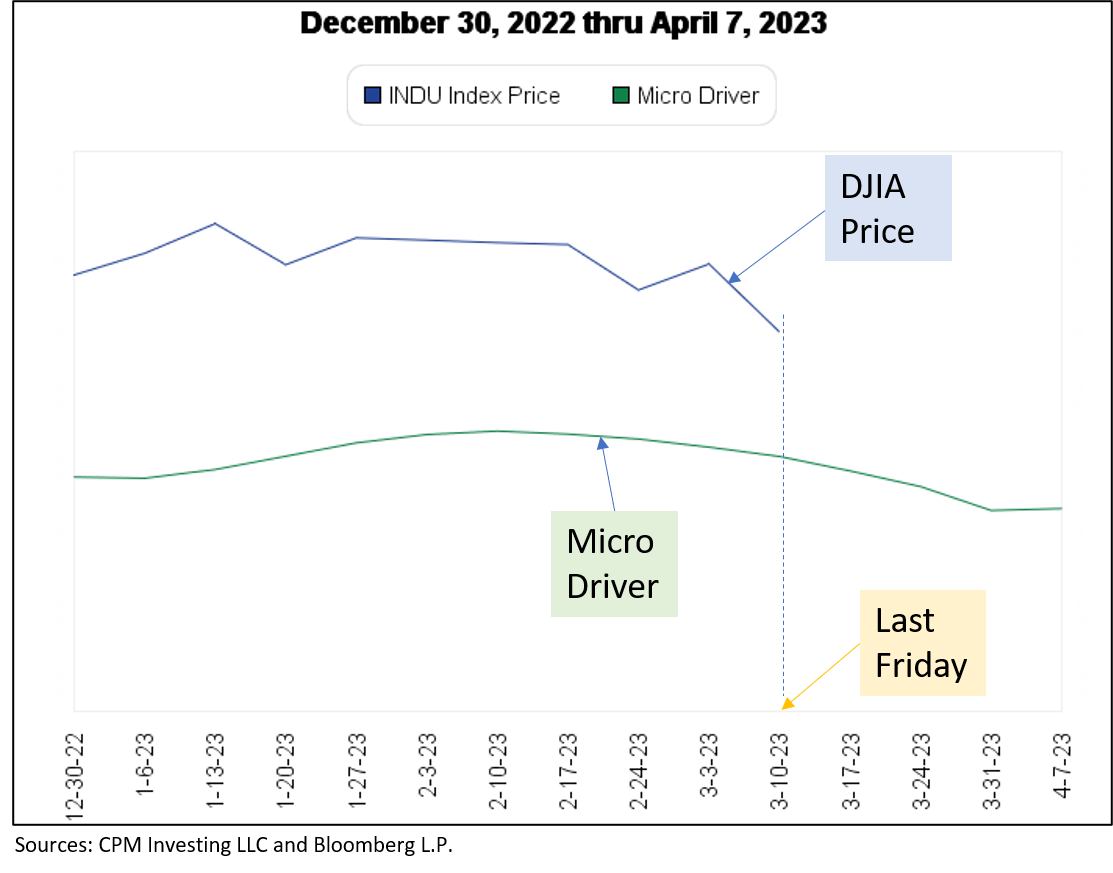

As a way of describing the dynamics of the last 15 months, I will first show the price of the DJIA (log scale) and its Macro, Exceptional Macro, and Micro MRI. Figure 1 below shows the period from December 1, 2020 through last Friday (April 7, 2023). The upper line is the DJIA, with a vertical line on April 7, 2023 in order to highlight the current date. The scale is not shown; the important patterns to see are the relative movements of the DJIA.

The smooth blue line is the Macro MRI. It peaked in December of 2021 (at the 80th percentile of levels since 1918), indicated by the red arrow. It has been in the downleg of its cycle until last week when it shifted to the upleg of its cycle (at the 27th percentile), indicated by the green arrow. If we were just making investment decisions based on the Macro MRI, we would have sold the DJIA-linked ETFs in December 2021 and we would be buying now.

Figure 1

However, our disciplines call for also considering the presence of the Exceptional Macro MRI and the cycles of the Micro MRI.

The small vertical arrows show the presence of the Exceptional Macro. It was present from the beginning of the period shown to July of 2021 (a), and a short period in December of 2022 and early 2023 (b). It appeared again two weeks ago.

The Exceptional Macro appears when the Macro MRI begins to shift from the downleg of its cycle to the upleg, although there are false signals from time to time. In many cases, when Exceptional Macro is present, the stock market is highly resilient and can overwhelm any vulnerability indicated by the Micro MRI.

In the current situation the Exceptional Macro is not as strong as it normally is after major stock price declines. This condition could be rooted in the fact that we have not had a major (e.g., a loss greater than 30%) decline in the DJIA thus far.

The purple line shows the Micro MRI for the DJIA, which tracks

its shortest cycle of resilience. One

can see that the DJIA price movements parallel the Micro MRI except when the

Exceptional Macro is present. As expected, the Exceptional Macro overwhelms any

lack of resilience stemming from the declining Micro MRI. From this perspective, the market has

performed as expected given the MRI conditions.

These dynamics suggest that the market will be more resilient for the next several weeks and possibly months:

- The Macro MRI for the DJIA is currently at a low level by historical norms (at the 27th percentile of levels since 1918), and has declined dramatically from the 80th percentile at its recent peak shown by the red arrow indicating the end of 2021,

- The Macro MRI has shifted to the upleg of its cycle as of the last week

- The last three times the DJIA’s Macro MRI troughed at this level (12/2020, 6/2016, and 9/1988) were followed 6 months later by returns of 15%, 10%, and 12%, respectively. In addition, the DJIA continued to move higher after the six-month period in each of these cases.

- The Exceptional Macro is present.

- The Micro MRI is a low level (34th percentile since 1918) in its normal range and is in the upleg of its cycle.

Consistent with these MRI dynamics, the algorithms and computer model evaluating this current status are inching closer to triggering a signal to buy our DJIA-linked ETFs. However, the strength of the Exceptional Marco is not as strong as it typically is at the end of the major stock market declines of the last 100 years. We are watching closely to see the persistence of the Exceptional Macro. It has appeared sporadically over the last several months and there is a small but meaningful chance that it ceases to be present over the next several weeks. If it ceases to be present, we will reduce our exposure to the riskiest ETFs. Yet, for reasons described below it seems that there is a good chance the resilience of the stock and bond markets will follow historical norms and increase from this point.

As you may recall from prior notes, we have identified likely drivers of the MRI. These drivers are based on objective variables that are exogenous to the markets and affect the collective risk aversion of investors. The key advantage of these drivers is that they can be forecast into the future giving an indication of future stock market resilience.

Figure 2 below shows the same period as the prior figure but includes up-arrows indicating the presence of the drivers. The small green up-arrows indicate the short-term driver and the larger blue up-arrows indicate the long-term driver. The short-term driver generally corresponds to the Micro MRI and the long-term generally corresponds to the Macro MRI.

Figure 2

As you can see in the Figure 2 above, the end of the long-term driver and the short-term driver in late 2021 correspond to the red arrow indicating the peak of the Macro MRI. The beginning of the long-term driver in approximately 8-5-2022 corresponded to a shift in DJIA (upper line) after which the DJIA moved more horizontally.

Conceptually, the effects of these drivers are additive and the long-term driver is stronger. When there are both green and blue arrows, we can expect investors to be more optimistic and the markets to be more resilient.

Figure 3 below is the same as prior figures with the

addition of diagonal arrows during periods when both the short- and long-term

drivers are present. During these

periods the DJIA avoided major declines and tended to move higher.

Figure 3

Subjectively, it appears that simply following the drivers might have been appropriate over the last 15 months; the MRI seemed to follow the drivers. However, following the MRI is typically more successful than following the drivers.

An example of this is the last time we had a major rate increases to fight inflation. The period from early 1981 through mid-1983 is similar to the current period. The period encompasses when Federal Reserve Chairman Paul Volker increased the Federal Funds rate to 20% from 11.2% in June 1981. The period also occurred during a period of low investor excitability. Figure 4 below shows the DJIA from December 1980 through April 1983 with the same markings used in the figures above. Volker increased rates at the point marked by letter A. That event coincidentally occurred at the end of the long-term driver (blue up-arrows), and occurred just before the peak in the Macro MRI, indicated by the red arrow.

Figure 4

The magnitude of the decline in the Macro MRI between the red arrow indicating the peak and the deep green arrow indicting the trough is coincidentally the same magnitude of the decline in the Macro MRI in the recent 15-month period. The change in the Macro MRI suggests that the market response to the recent rate hikes has been as aggressive as it was to the Volker rate hikes decades earlier.

Subjectively, it appears that from the red arrow to the end of the period shown in Figure 4, the DJIA appears to follow the MRI as opposed to the drivers; the drivers were less explanatory of the change in the DJIA price. This is confirmed by a statistical analysis we performed using the drivers and data from the Daily News Sentiment Index produced by the US Federal Reserve Bank of San Francisco. The conclusions from this analysis are:

- During the Volker period, the Daily News Sentiment Index explained a high level (77%) of the variations on the DJIA. The MRI capture the effects of news sentiment. The drivers explained a far lower level (23%).

- During the recent period, the drivers explained a higher level (55%) of the variation in the DJIA. The Daily News Sentiment Index explained less (45%).

While the periods were similar in that they both were affected by large hikes in interest rates to combat inflation and occurred during periods of low investor excitability, the rate change in June of 1981 came after a decade of high interest rates and was more extreme in terms of a rate change. Also, a 20% short-term interest rate is conceivably more economically traumatic and newsworthy than a 4.8% rate. Perhaps the market consensus after the initial shock of inflation and rate increases is that the current period is less traumatic and will pass more quickly.

The less traumatic nature of the recent period is supported

by the performance of the DJIA in both periods. Figure 5 below shows the price

level of the DJIA in the two periods when interest rates increased

dramatically. From the peak in the DJIA through the lowest point in the DJIA

for the most recent period (red line) is at week 39, the two paths are

similar. After that point, the declines

for the 1981 period continued while there has been a rebound in the recent

period.

Figure 5

US Treasury Bonds

During most periods over the last 100 years, bonds have tended tend to move higher when stocks move lower. It is this relationship the makes a portfolio that mixes stocks and bonds attractive. However, in times of rising interest rates that are likely to induce lower economic growth (like the Volker and the current periods), bonds and stocks may drop at the same time.

Our least aggressive bond ETF is SHY, which is linked to a

1- to 3-year US Treasury bond index. Figure 6 below shows in the upper panel

the performance (on a log scale) of a 2-year US Treasury bond index, which is a

useful proxy for SHY. The period shown is since January of 2000 through last

Friday. In the lower panel is the Macro MRI. The vertical green lines in both

panels are the Exceptional Macro MRI.

Figure 6

You can see that over most of the time period shown, the index in the upper panel moves higher, which indicates a positive return for the index. The index moved higher even in many cases when the Macro MRI moved lower. This is because of the yield on the bonds and has meant that this index and the related ETFs are good investments in most market environments. This behavior makes SHY a good default investment when other ETFs lack resilience.

In most periods covered in Figure 6, the appearance of the Exceptional Macro indicated the beginning of a period of higher resilience and returns. In the lower panel, the appearance of the Exceptional Macro indicated a likely beginning of the Macro MRI moving higher, as expected. Recently, the Macro MRI peaked recently at the red arrow in the lower panel. The red arrow is also shown in the upper panel. It was clear at this time that interest rates would be rising to fight inflation and this made SHY unattractive as a default investment. It made sense during this period to use higher Box #2 Cash levels as a default investment.

The important observation in Figure 6 above is that the Macro MRI has recently begun the upleg of its cycle and has done so at a low level (green arrow). The Macro MRI is currently at the 1st percentile of levels since the beginning of the index in 1980 – an extremely low level. We now expect SHY to function more normally as a default investment and we have taken Box #2 Cash down to a normal level.

A similar pattern is seen for the 10-year US Treasury bond index that is a good proxy for our more aggressive bond ETFs (UST and TYD), as seen in Figure 7 below. At the end of 2020 shown by the red arrow below, the Macro MRI was at the 100th percentile since the beginning of the index in 1983. It declined to a percentile of lower than the 1st percentile at the time shown by the deep green arrow.

Figure 7

Based on analysis of yields for the 10-year bonds (which has

a longer history), the magnitude of change in Macro levels shown above would be

equally extreme over the period since 1962.

The current level of the Macro MRI would be similar to the levels in the

fall of 1963, early 1970, late 1966, and late 1981. These are all time times

after which bonds produced high returns.